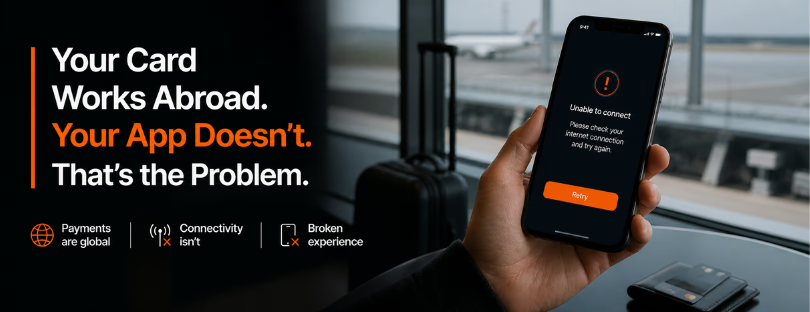

Your Card Works Abroad. Your App Doesn’t

You land. You turn your phone on. You open your banking app to check if that airport taxi overcharged you. banking app not working abroad

And suddenly… nothing works.

The card went through. The payment was approved. The money is gone.

But the app? Frozen. Loading. Timing out. Asking for verification codes that never arrive.

This is the quiet contradiction no one in fintech really wants to talk about.

Payments are global.

Connectivity isn’t.

And that gap is breaking the entire user experience.

The illusion of “Global banking”

Let’s start with what actually works.

Your card. Whether it’s from a traditional bank, a neobank, or a fintech app, it will almost always work abroad. That’s because the payment infrastructure is built for it.

Visa. Mastercard. Global acquiring networks. Decades of optimization.

You tap in Tokyo, pay in New York, withdraw in Paris. It just works.

From a payments perspective, we’ve solved globalization.

But here’s where things quietly fall apart.

Everything around the payment still depends on connectivity.

And connectivity is still fragmented, inconsistent, and often unreliable.

The moment things break

The real problem doesn’t show up when you pay.

It shows up right after.

You open your app to:

- Check the transaction

- Freeze your card

- Approve a security prompt

- Get a one-time password

- Transfer money

- Contact support

And suddenly, you’re stuck.

No data. Weak signal. Roaming delays. SMS codes arriving late or not at all.

Or worse, your app flags the login as suspicious because you’re in a new country… and now you need to verify yourself using a connection you don’t have.

It’s not a rare edge case.

It’s the default experience for millions of travelers.

Connectivity is still treated as “someone else’s problem.”

This is where most banks and fintech apps get it wrong.

They’ve built incredible payment experiences.

But they’ve outsourced connectivity to… chance.

- The user has roaming

- The user has Wi-Fi

- The user will figure it out

- Roaming is expensive or disabled

- Public Wi-Fi is unreliable or insecure

- Local SIM cards are inconvenient

- Even eSIM users can face activation gaps

So what happens?

The user is left in a dead zone between “payment works” and “app doesn’t.”

And that’s where trust starts to erode.

Security makes it worse, not better

Ironically, the more secure the system is, the more fragile it becomes abroad.

Think about it.

Banks rely heavily on:

- SMS verification codes

- Push notifications

- Real-time app approvals

- Location-based fraud detection

All of these assume stable connectivity.

But when connectivity is unstable, security becomes friction.

You get:

- Locked out of your account

- Stuck transactions

- Failed logins

- Endless retry loops

From the bank’s perspective, this is “working as intended.”

From the user’s perspective, it feels broken.

The hidden cost of a broken experience

This isn’t just a minor inconvenience.

It has real consequences.

Users start to:

- Avoid using certain cards abroad

- Carry backup cash “just in case”

- Disable security features

- Switch to competitors that “just work”

And here’s the bigger issue.

The brand damage doesn’t show up in a support ticket.

It shows up in behavior.

Quietly.

Over time.

A bank can invest millions into UX, onboarding, and features…

…and still lose the moment a user lands in another country.

Neobanks are especially exposed

If you’re a digital-first bank, this problem hits even harder.

Because your entire relationship with the user is inside the app.

No branches. No fallback.

If the app doesn’t work, you don’t exist.

That’s a brutal reality.

Traditional banks at least have brand inertia. Neobanks don’t.

So when connectivity fails, the experience collapses completely.

The expectation gap

Here’s what users expect today:

“If my card works globally, everything should work globally.”

That feels obvious.

But it’s not how the system is designed.

Payments are built on global rails.

Apps are built on local connectivity.

And that mismatch creates a broken expectation.

Users don’t think in terms of infrastructure layers.

They just see a product that works halfway.

Your customers will buy connectivity. The question is: from you, or from someone else?

We help airlines, banks, and travel platforms turn that demand into a built-in product — not a missed opportunity.

eSIM is part of the answer, but not the full story

This is where eSIM enters the conversation.

Because at its core, this is a connectivity problem.

eSIM makes it easier to get data abroad:

- No physical SIM swapping

- Instant activation

- Multi-country coverage

- More predictable pricing than roaming

But even here, there’s a gap.

Most users still:

- Buy eSIMs reactively (after landing)

- Struggle with setup

- Don’t know which provider to choose

- End up with fragmented experiences

So while eSIM solves the technical problem, it doesn’t fully solve the user journey.

The real shift: connectivity as part of the product

This is where things get interesting.

The next generation of fintech won’t treat connectivity as external.

They’ll integrate it.

Directly.

Imagine this:

You open your banking app before a trip.

And instead of a travel notice, you get:

“You’re going to Italy. Do you want seamless connectivity while you’re there?”

One tap.

Done.

No separate app. No comparison. No confusion.

Now your app works exactly the same abroad as it does at home.

That’s the shift.

Connectivity becomes part of the financial product.

Not an afterthought.

Why hasn’t this happened yet

Two reasons.

First, complexity.

Connectivity involves:

- Telecom partnerships

- Regulatory requirements

- Device compatibility

- Global coverage agreements

It’s not trivial.

Second, ownership.

Banks don’t see themselves as connectivity providers.

Telcos don’t see themselves as part of fintech UX.

So the problem sits in the middle.

Unclaimed.

Unsolved.

But the opportunity is massive

Whoever solves this properly wins more than just convenience.

They win:

- Daily engagement

- Trust in critical moments

- Differentiation in a crowded market

- A deeper role in the user’s travel experience

Because travel is where products get tested hardest.

If you work there, you work everywhere.

Quietly, partnerships are already happening

We’re starting to see early signs.

Some fintechs are exploring:

- Embedded eSIM offers

- Travel data bundles

- Connectivity perks for premium users

And on the other side, connectivity platforms are opening APIs that make this integration possible.

This is where things like the eSIM Partner API come into play.

Instead of building telecom infrastructure from scratch, banks can plug into existing global connectivity layers.

Faster.

Simpler.

More scalable.

But most are still early.

Which means the gap is still wide open.

This is not about data. It’s about reliability

Let’s be clear.

Users don’t care about gigabytes.

They care about one thing:

“Will this work when I need it?”

At the airport. At the hotel. During a payment. In a moment of stress.

That’s the real product.

Reliability.

And right now, that reliability breaks the moment connectivity drops.

The bottom line banking app not working abroad

Your card working abroad is no longer impressive.

It’s expected.

Is your app not working?

That’s unacceptable.

And the gap between those two realities is where the next wave of innovation will happen.

Not in payments.

Not in features.

But in making the entire experience actually work, everywhere.

Because global payments without global connectivity…

isn’t really global at all.