Travel eSIM Economics: Why Repeat Users Matter

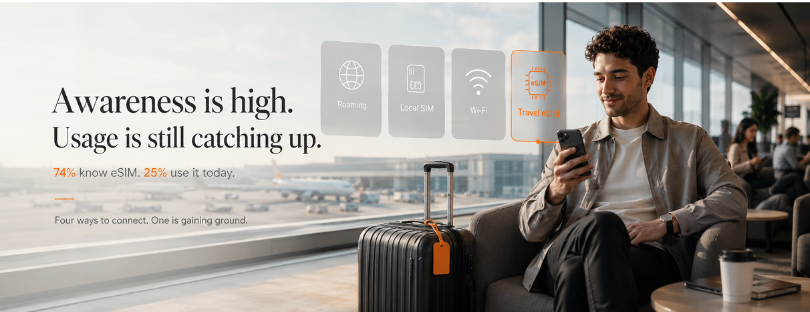

The travel eSIM market looks beautifully simple from the outside.

A traveler opens an app, buys a $10 or $20 data plan for Japan, Spain, the United States, or Thailand, scans a QR code or installs the eSIM instantly, and lands connected. No roaming shock. No SIM kiosk. No airport Wi-Fi panic.

That is the story customers see.

Behind the scenes, the economics are much tougher.

The real battle in travel eSIM is not only coverage, price, or how many countries appear on a provider’s homepage. The real battle is Customer Acquisition Cost versus Customer Lifetime Value.

Or, in simpler terms: how much does it cost to win a traveler, and how many times will that traveler come back?

That question may decide who survives the next phase of the travel eSIM market.

The first sale is expensive

Travel eSIM companies sell low-ticket products in a very expensive digital environment.

A customer might buy a $7 weekend plan, a $12 regional plan, a $20 country package, or a $35 larger data bundle. From the traveler’s point of view, that feels convenient and affordable.

From the provider’s side, it can be painfully thin.

To win that customer, the company may have paid for Google Ads, App Store visibility, influencer campaigns, SEO content, affiliate commissions, cashback offers, referral bonuses, PR, social media, or partnerships with travel platforms.

None of that is free.

And because digital advertising works like an auction, costs rise when more players enter the market. The travel eSIM category has become crowded, which means providers are often competing for the same traveler at the same moment: right before a trip, when purchase intent is high.

That is valuable traffic. It is also expensive traffic.

So the hard question is this: if a provider spends $20, $30, or more to acquire a customer, but that customer buys only one $15 eSIM, where is the profit?

Often, it is not in the first transaction.

Why CAC hurts travel eSIM brands

Customer Acquisition Cost, or CAC, is the amount a company spends to bring in a new customer.

The simple formula is:

Total marketing and sales spend divided by new customers acquired.

In travel eSIM, that cost can include paid search, social ads, affiliate commissions, content marketing, app store optimization, influencer deals, partnerships, and technical onboarding flows.

The problem is not that these channels are bad. Many of them work extremely well.

The problem is that they reset the economics every time a traveler behaves like a one-time buyer.

This is where travel eSIM is different from traditional telecom.

A mobile operator usually tries to acquire a customer into a recurring relationship. A monthly plan, a family bundle, a contract, a prepaid top-up habit, or a multi-service package gives the operator time to recover acquisition cost.

Travel eSIM is more episodic.

Someone buys an eSIM for Turkey in July, another for the United States in November, then nothing for months. They may return to the same provider. Or they may search again and choose whoever appears first, cheapest, or most recommended that day.

That behavior creates a dangerous loop.

If the brand has to reacquire the same type of customer again and again, it is not really building a customer base. It is renting demand.

LTV is where the real business begins

Customer Lifetime Value, or LTV, measures how much revenue a customer may generate over the full relationship with a company.

In the simplest version, it is average revenue per user multiplied by the expected customer lifespan. More advanced models also consider gross margin and churn.

For travel eSIM providers, LTV improves when customers come back.

That can happen through repeat trips, regional bundles, global plans, app loyalty, stored payment details, saved devices, credits, wallets, business travel use, second-device connectivity, or annual data packages.

This is why the second purchase matters so much.

The first purchase proves demand.

The second purchase proves trust.

The third purchase starts to change the economics.

A provider that turns a one-time buyer into a repeat customer can afford higher acquisition costs. A provider that cannot do that remains exposed to advertising inflation, affiliate dependency, and price pressure.

This is why the CAC/LTV equation is much more than a finance metric. It is a strategy test.

The retention race has started

Many travel eSIM companies are already trying to solve this problem.

Some are building apps that act like permanent travel companions. The goal is not just to sell one eSIM, but to stay installed on the customer’s phone between trips.

That explains features such as saved payment methods, top-up reminders, global wallets, automatic plan suggestions, destination-based notifications, and easier reinstallation flows.

Others are moving toward annual or recurring plans. Instead of selling data only when someone travels, they are trying to create baseline connectivity that stays active throughout the year.

That model is especially interesting for frequent travelers, remote workers, business users, second phones, tablets, connected laptops, travel routers, and families managing multiple devices.

Then there is embedded distribution.

This may be the most powerful path of all.

If an eSIM offer is integrated into an airline app, fintech wallet, travel booking platform, OTA, bank, hotel loyalty program, or device ecosystem, the economics can change dramatically.

The provider no longer has to fight for every customer through paid search. Connectivity becomes part of a broader travel journey.

That is a very different business.

It means the eSIM provider is not just selling data. It is becoming infrastructure inside someone else’s customer relationship.

Scale changes the game

The CAC versus LTV equation also explains why scale matters so much in travel eSIM.

Larger providers can spread brand investment across more users. They can negotiate better wholesale terms. They can test more acquisition channels. They can afford stronger apps, better customer support, and broader market visibility.

Smaller providers can still win, but they need sharper positioning.

Competing only on cheap gigabytes is dangerous because pricing can be copied. Coverage claims can be copied. Destination pages can be copied. Even “global connectivity” messaging can be copied.

What is harder to copy is owned demand.

That can come from a loyal audience, a trusted brand, a strong B2B distribution network, a niche use case, a superior retention model, or a product that solves a very specific connectivity problem better than generic providers.

In other words, smaller providers do not necessarily need to outspend the biggest players.

But they do need to avoid becoming invisible in a market where everyone is bidding for the same traveler.

Affiliate traffic is useful, but not enough

Affiliate marketing has played a major role in the growth of travel eSIM.

That makes sense. Travelers search before they buy. They compare countries, prices, data limits, validity, unlimited plans, hotspot rules, app experience, and reviews. Publishers, comparison sites, influencers, and travel blogs help convert that demand.

For providers, affiliates can be an efficient acquisition channel because payment is often tied to performance.

But there is still a strategic risk.

If a provider depends too heavily on third-party traffic, it does not fully control the customer relationship. The customer may remember the comparison site, the discount code, or the search result more than the eSIM brand itself.

That is fine for short-term growth.

It is weaker for long-term defensibility.

The strongest providers will use affiliate and paid channels to acquire customers, but then work hard to convert those customers into direct, repeat users.

That is where app experience, support, trust, reliability, payment convenience, and post-trip engagement become important.

The future belongs to demand owners

The next phase of travel eSIM will not be decided only by who offers the cheapest 10GB plan for Europe.

That layer is already crowded.

The real winners will be the companies that solve the CAC versus LTV equation better than everyone else.

Some will do it through strong consumer brands. Some will do it through embedded partnerships. Some will do it through annual plans, business travel products, second-device connectivity, or enterprise mobility. Others may win by owning a specific niche instead of trying to be everything to everyone.

But the direction is clear.

The travel eSIM market is moving from one-off transactions toward longer customer relationships.

That is a major shift.

For years, the category was marketed as a quick roaming alternative: cheaper than roaming, easier than a local SIM, faster than airport Wi-Fi.

That message helped the industry grow.

But it may not be enough to build the next generation of profitable eSIM companies.

The real question now is not simply: can you sell a traveler an eSIM?

It is: can you make that traveler come back without paying for them all over again?

That is where the market will separate.

The companies that keep renting attention will remain trapped in a CAC spiral. The companies that control demand, build trust, and create repeat connectivity habits will have a much stronger future.

In the end, the travel eSIM winners will not just sell data.

They will own the relationship around connectivity.