Half of Customers Are Asking: What Am I Really Paying My Telco For?

There is an uncomfortable sentence sitting inside Simon-Kucher’s Global Telecom Study 2026: telcos are not necessarily overpriced. They are failing to justify the price.

For years, operators could defend premium pricing with familiar arguments: better network, stronger brand, better stores, safer support, maybe a handset deal on top. But the 2026 market looks different. Simon-Kucher’s study, based on 17,985 consumers across 35 countries, shows how much of the old premium playbook has leaked into the low-cost market.

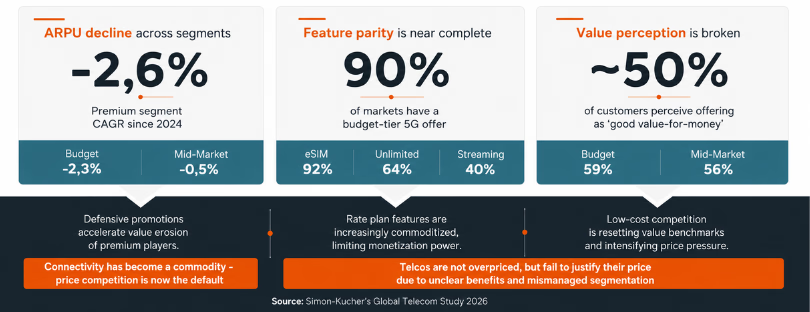

In 90% of markets analysed, at least one budget player already offers 5G. In 92%, budget players offer eSIM. Apps are common. Unlimited data is no longer exotic. Even streaming bundles, once a nice premium add-on, are showing up in budget propositions in 40% of markets.

So when customers compare a premium plan with a cheaper one, the question is no longer “which one has the modern features?” It is “Why exactly am I paying more?”

The Commodity Trap

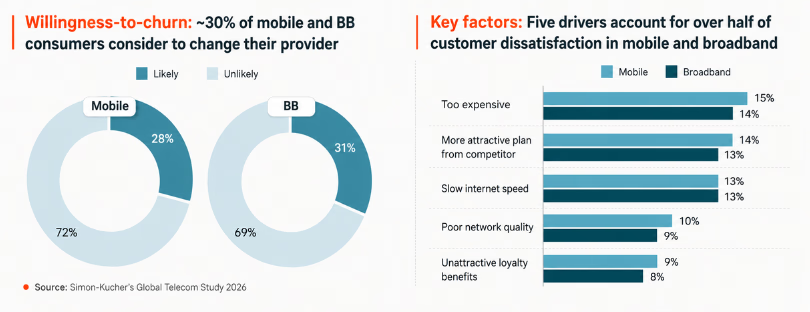

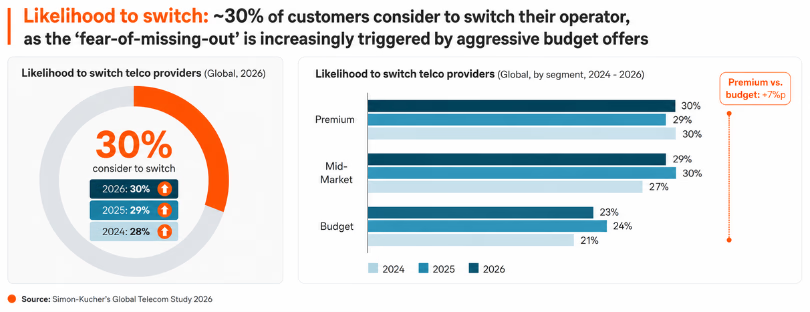

Simon-Kucher describes connectivity as increasingly commoditized, and that is not consultant language for drama. It is visible in customer behaviour. Only around half of customers see telecom services as good value for money. Around 30% of mobile and broadband customers say they are likely to switch providers. The premium segment has not escaped this pressure. In fact, premium customers show a higher willingness to churn than budget customers.

That sounds counterintuitive until you think like a normal customer. A budget customer expects limits. A premium customer expects relief. If the app is confusing, support is slow, roaming is unclear, loyalty benefits feel pointless, and the bill still creeps upward, the premium label starts to feel decorative.

This is why the report’s most important message is not “cut prices.” It is “fix value perception before touching price.” Price is often the visible complaint, but the deeper issue is whether people understand what they are getting.

GSMA’s Mobile Economy 2026 adds useful context here: mobile technologies generated $7.6 trillion for the global economy in 2025, while 5G, AI and digital services are expected to drive the sector’s next growth phase. The mobile industry is still structurally important. The problem is that importance does not automatically translate into affection, loyalty, or willingness to pay more.

Features Are Not Enough

A few years ago, offering eSIM could still make a provider feel advanced. Today, eSIM is becoming table stakes. For travelers, the shift is sharper. GSMA Intelligence reported that across 11 major countries surveyed, 12% of consumers who travelled internationally in the previous year used eSIM abroad. It also noted that travel eSIMs are increasingly appearing inside travel and finance journeys, including booking platforms and packaged bank accounts.

That matters because operators are no longer competing only with other operators. They are competing with travel eSIM apps, banks, booking platforms, loyalty programs, super apps and device ecosystems. Airalo, Ubigi, Yesim, Nomad eSIM, Saily and similar providers have trained many travelers to expect instant purchase, clear destination pricing and simple setup. Not all of these services are perfect. Some vary by destination, speed, validity, hotspot rules or support quality. But they did one thing very well: they made roaming feel understandable.

The future premium plan cannot simply say “5G, eSIM, unlimited, app.” A budget provider can say that too. A stronger proposition says: your family plan is simple, your roaming rules are clear, your support is fast, your phone upgrade is predictable, your data works where you actually travel, and your loyalty benefits are not random coupons hiding in an app nobody opens.

The future premium plan cannot simply say “5G, eSIM, unlimited, app.” A budget provider can say that too. A stronger proposition says: your family plan is simple, your roaming rules are clear, your support is fast, your phone upgrade is predictable, your data works where you actually travel, and your loyalty benefits are not random coupons hiding in an app nobody opens.

Loyalty Becomes Infrastructure

One of the more interesting findings in the Simon-Kucher study is how strongly engagement links to value. Telco app usage is associated with a 17% uplift in customer lifetime value. Loyalty program participation is linked to a 20% uplift. That does not mean operators should stuff every app with banners and badges.

It means the app can become more than a digital bill drawer. It can be the place where a customer sees usage, understands the plan, receives a better roaming option before travel, upgrades a device, adds security, manages family members, or gets a fair retention offer before frustration turns into churn.

Deloitte’s 2026 Telecommunications Industry Outlook points in the same direction, arguing that operators need to move from product-centric models toward value ecosystems built around personalization, proactive service and seamless digital experiences. It also highlights eroding loyalty and weak perceived differentiation across telecom brands.

Deloitte’s 2026 Telecommunications Industry Outlook points in the same direction, arguing that operators need to move from product-centric models toward value ecosystems built around personalization, proactive service and seamless digital experiences. It also highlights eroding loyalty and weak perceived differentiation across telecom brands.

This is where the good operators separate themselves from the noisy ones. AI support can help, but only if it reduces friction. Loyalty can help, but only if it feels useful. Bundles can help, but only if they are coherent. A customer who only wants the cheapest SIM-only plan is not asking for an ecosystem. They want simplicity and price discipline. A frequent traveler, family manager, remote worker or enterprise user may value something richer, but only if the benefit is obvious.

The Mid-Market Moment

The study also suggests that mid-market operators may be in a surprisingly strong position. They are not trapped by the same premium expectations, but they can still offer credible service. That is exactly where many modern connectivity propositions now live: not luxury, not bargain-basement, but clear, flexible and low-friction.

This is why multi-brand strategy matters. If a premium operator fights every low-cost challenger with discounts under the same brand, it teaches customers to wait for promotions. If it ignores budget competition, it leaves the bottom of the market open to MVNOs and digital-first challengers. A separate brand or sub-brand can work, but only if the roles are clear. Otherwise, the company ends up competing with itself.

The same logic applies in travel connectivity. Operators can compete directly on roaming price, partner with travel eSIM platforms, launch their own travel eSIM offers, or bundle international data into premium tiers. There is no single best answer. But pretending that traditional roaming will stay protected is not a strategy.

Conclusion about telco customer loyalty

The most useful line in Simon-Kucher’s report is also the most uncomfortable: “Winner telcos don’t sell SIM cards – they sell ecosystems.”

That does not mean every operator should become a lifestyle marketplace. Some should do less, but do it cleaner. Some should build sharper sub-brands. Some should partner with travel platforms or fintechs instead of trying to own every customer journey alone. Some should focus on enterprise-grade reliability, security and support, where low-cost challengers are weaker.

The broader market is moving in the same direction. GSMA sees mobile growth increasingly tied to 5G, AI and digital services. Deloitte sees loyalty and value perception becoming central to telecom strategy. Travel eSIM providers are showing how fast customer expectations can change when setup and pricing become easier.

For operators, the real 2026 question is not whether customers still need connectivity. Of course they do. The question is whether they believe their provider adds value beyond the signal bar. If the answer is no, another provider, app, bank, airline or booking platform will be very happy to explain it for them.