Who Owns the Customer in Travel Connectivity?

Everyone says they want to “own the customer.”

In travel connectivity, that sentence is already outdated.

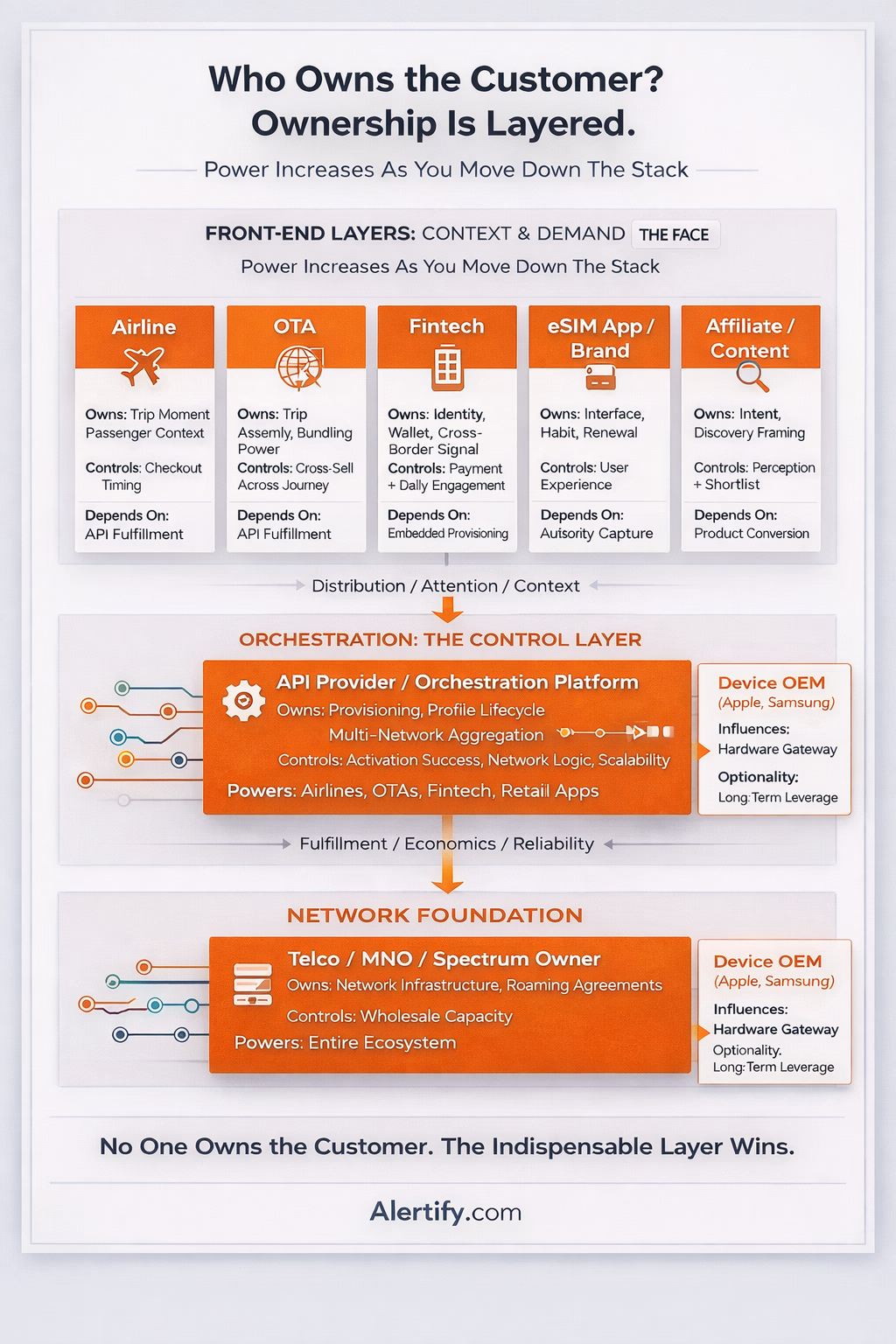

There is no single customer relationship anymore. There is a layered stack:

Discovery

Booking

Payment

Provisioning

Network delivery

Support

Renewal

Different players control different layers. The power question is not who owns the customer.

It is who controls the most strategic layers — and who is quietly becoming indispensable.

Because in this market, indispensability beats visibility.

The front-end illusion: brand does not equal control

Travel eSIM apps look like they own the customer.

They have:

- The app icon

- The login

- The push notifications

- The visible balance

But most of them do not have demand.

Demand is shaped upstream by:

Affiliates controlling comparison framing.

Airlines are embedding connectivity at checkout.

OTAs are bundling it inside the trip assembly.

Fintech apps are normalizing it next to FX and travel perks.

Apps often control the interface. They do not always control the funnel.

And in digital markets, whoever controls the funnel dictates pricing pressure.

Front-end visibility is not structural ownership.

Not all travel eSIM providers sit at the same structural layer. Some operate primarily as retail brands fighting for user acquisition. Others control orchestration or embedded API distribution and are therefore far less vulnerable to bundling pressure.

Airlines: control of context, not infrastructure

Airlines hold the trip moment.

They know where you’re going.

They know when you’re landing.

They know your loyalty tier.

Connectivity offered inside booking flows converts because intent is guaranteed.

But airlines rarely want to manage telecom complexity.

They do not want:

Provisioning failures

Roaming disputes

Cross-border regulatory friction

Network blame

So they outsource the infrastructure.

They own context and trust.

Someone else owns the rails.

This is contextual ownership — powerful, but dependent.

OTAs: the quiet bundling power

Booking.com, Expedia and Trip.com operate at a broader altitude than airlines.

They assemble the entire journey.

Flights.

Hotels.

Transfers.

Insurance.

Experiences.

When connectivity becomes another “travel utility” add-on, OTAs gain structural leverage.

They see cross-vertical behavior.

They see multi-trip patterns.

They can bundle data into loyalty and rewards logic.

They may never become telecom operators.

But they can normalize connectivity as a default trip component.

Bundling creates dependency.

Dependency creates power.

Fintech: the most underestimated owner

Revolut and Wise already own the most sensitive layer: money.

They know:

When FX spending starts.

When airport transactions occur.

How frequently do you travel?

Which currencies dominate your profile?

If connectivity sits inside a fintech app, it becomes invisible infrastructure.

Not a product.

Not an upsell.

Just a toggle next to insurance and currency exchange.

Fintech owns:

Identity.

Payment.

Daily usage habit.

If they embed provisioning through APIs, they do not need telecom expertise.

They simply wrap it inside a financial ecosystem.

That is structural capture.

And most travel eSIM brands are not prepared for that competition.

Affiliates: control of perception

Affiliates control intent.

When someone searches “best eSIM for Japan,” the shortlist is shaped before the purchase even begins.

Affiliates define:

What “reliable” means.

What “unlimited” means.

Which trade-offs matter?

They rarely own lifetime retention.

But they shape first trust.

In a fragmented market, first trust determines pricing elasticity.

Whoever defines the category language exerts soft power over the entire ecosystem.

API and orchestration providers: the real gravity center

This is where ownership becomes structural.

Infrastructure enablers control:

Remote SIM provisioning

Profile lifecycle management

Multi-network aggregation

Coverage logic

Wholesale exposure

They influence activation success.

They influence margin.

They influence scalability.

They power multiple brands simultaneously.

If a single orchestration layer supports airlines, fintech apps, OTAs, and white-label travel brands, that layer becomes a choke point.

And choke points create gravity.

Customers may never know their name.

But the market will depend on their uptime.

In platform markets, the rails accumulate power faster than the storefronts.

Telcos: own the spectrum, not the relationship

Traditional operators still control spectrum and roaming agreements.

But travel connectivity increasingly bypasses their retail channels.

They supply wholesale capacity.

Others package it.

They own the network.

They do not always own the traveler.

That shift compresses retail leverage and pushes telcos toward B2B infrastructure roles.

OEMs: the hardware gatekeepers

Apple and Samsung control the hardware layer where eSIM lives. travel connectivity customer ownership

They define:

Default carrier prompts

eSIM management interfaces

Secure element integration

OS-level connectivity logic

If OEMs deepen carrier selection or embedded connectivity flows at OS level, discovery could shift again.

Hardware control is long-term optionality.

They do not need to move aggressively today to remain structurally powerful tomorrow.

Consumer vs enterprise: two different ownership games

In consumer travel eSIM, ownership revolves around:

Brand.

Habit.

Convenience.

Pricing comparison.

Embedded distribution.

In enterprise travel risk and mobility management, ownership revolves around:

Visibility.

Control.

Policy orchestration.

Centralized dashboards.

Cost governance.

Enterprises do not care who has the prettiest app.

They care who can show, in real time, who is connected, where, and at what cost.

That shifts ownership toward orchestration layers, not retail brands.

Consumer markets reward distribution dominance.

Enterprise markets reward control layers.

Different power maps.

Different winners.

The conclusion: where this actually ends

The market looks fragmented today. It won’t stay that way.

Travel connectivity is moving toward vertical compression.

The layer that controls identity, payment, and provisioning in one integrated loop will gradually squeeze the others.

Here’s where the economic pressure builds:

Retail travel eSIM apps are the most exposed.

They face rising acquisition costs from affiliates.

They face bundling pressure from OTAs.

They face embedded distribution from airlines.

They face ecosystem capture from fintech.

If they do not move upstream into distribution partnerships or downstream into infrastructure control, they become replaceable front ends.

Airlines and OTAs are structurally stronger because they own context and trip assembly. But even they depend on external orchestration layers. Their leverage lasts only as long as infrastructure remains modular.

Fintech is the dark horse. It already owns identity, payment rails, daily app engagement, and cross-border data signals. If it deepens provisioning control instead of remaining a reseller wrapper, it can compress margin across the stack.

And then there is the infrastructure layer.

API orchestration providers accumulate silent power. They sit beneath airlines, OTAs, fintech apps, white-label travel brands, and even enterprise mobility platforms. If consolidation happens, it will likely happen here first.

This is the structural reality:

In consumer travel, distribution power wins first.

In enterprise mobility, orchestration power wins decisively.

Over the next three to five years, expect three shifts:

- Connectivity becomes a default trip utility inside OTAs and airline ecosystems.

- Fintech integrates travel connectivity deeper into financial loyalty stacks.

- Infrastructure layers consolidate quietly, reducing the number of true orchestration backbones powering the market.

When that happens, “owning the customer” will no longer mean having the biggest logo on the checkout page.

It will mean controlling the layer that others cannot remove without breaking their product.

In travel connectivity, ownership does not belong to the loudest brand.

It belongs to the indispensable layer. travel connectivity customer ownership

And indispensability always beats visibility.