There was a time when a “payment app” meant splitting dinner with a friend or tapping your phone at a coffee shop. That feels almost old-fashioned now. The best mobile payment apps are no longer just payment tools. They are becoming travel wallets, loyalty layers, cross-border money movers, identity shortcuts and, in some cases, miniature banks sitting inside your phone.

That shift matters for travellers. When you land in another country, your phone is usually the first thing you reach for: to call a ride, check into a hotel, buy a train ticket, order food, pay for data, or send money back home. Connectivity and payments now live side by side. If one fails, the whole travel experience feels broken.

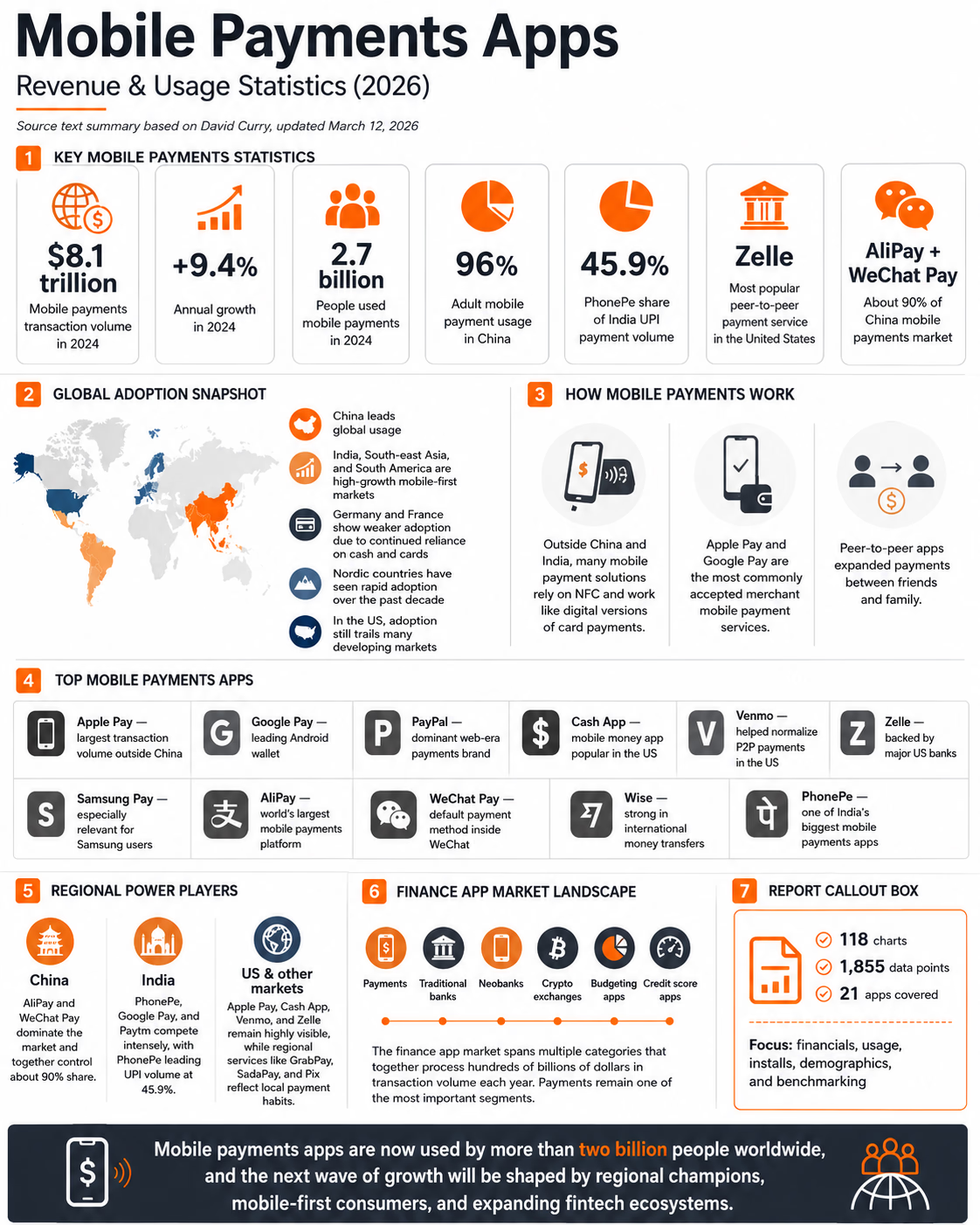

Worldpay’s Global Payments Report shows how far this has moved. Digital payments grew from 34% of global e-commerce value in 2014 to 66% in 2024, while in-store digital payments rose from 3% to 38% over the same period. Digital wallets such as Apple Pay, Google Pay, PayPal and WeChat Pay are now treated as mainstream payment methods, not “alternative” options.

Apple Pay

Apple Pay remains one of the cleanest mobile payment experiences, especially for iPhone users. Its strength is not that it tries to do everything. It is that it disappears into the device. You double-click, authenticate, tap, and move on.

For travellers, that simplicity is powerful. Apple Pay works well in markets where contactless card acceptance is strong, especially across Europe, the UK, North America, Australia and parts of Asia. It is also widely used for online checkout, transit systems, airline apps, hotel apps and food delivery.

The real advantage is trust. Apple controls the hardware, operating system and wallet experience, which gives Apple Pay a very strong position at the device layer. The downside is obvious: it is mainly useful if you are already inside the Apple ecosystem. For Android-heavy markets, Apple Pay is not the default behaviour.

Google Wallet

Google Wallet is Apple Pay’s natural counterpart for Android users, but with a slightly different personality. It is less about a closed premium ecosystem and more about broad device reach. For travellers using Android phones, Google Wallet is usually the most practical tap-to-pay option.

Its value is not only payment. Google Wallet can also hold boarding passes, transport cards, loyalty cards and other digital credentials depending on country and issuer support. That makes it useful in the messy middle of travel: airports, ticket machines, taxis, supermarkets, tourist attractions and hotel check-ins.

The challenge is fragmentation. Android markets vary widely by bank support, merchant infrastructure and local payment habits. Google Wallet can feel excellent in one country and oddly limited in another. Still, for most Android travellers, it belongs at the top of the list.

PayPal

PayPal is still one of the most important payment apps because it owns a different part of the journey: online trust. It is especially useful when paying merchants you do not know well, booking services abroad, shopping internationally, or sending money across borders.

PayPal says its digital wallet lets users pay friends, family, sellers, and businesses, send money across PayPal and Venmo, and send money to more than 110 countries. That makes it more global than many domestic payment apps, even if fees and exchange rates need to be checked carefully.

For travellers, PayPal is less about tapping at the terminal and more about confidence at checkout. It is the app you use when a website looks legitimate but unfamiliar. That is still a very real use case.

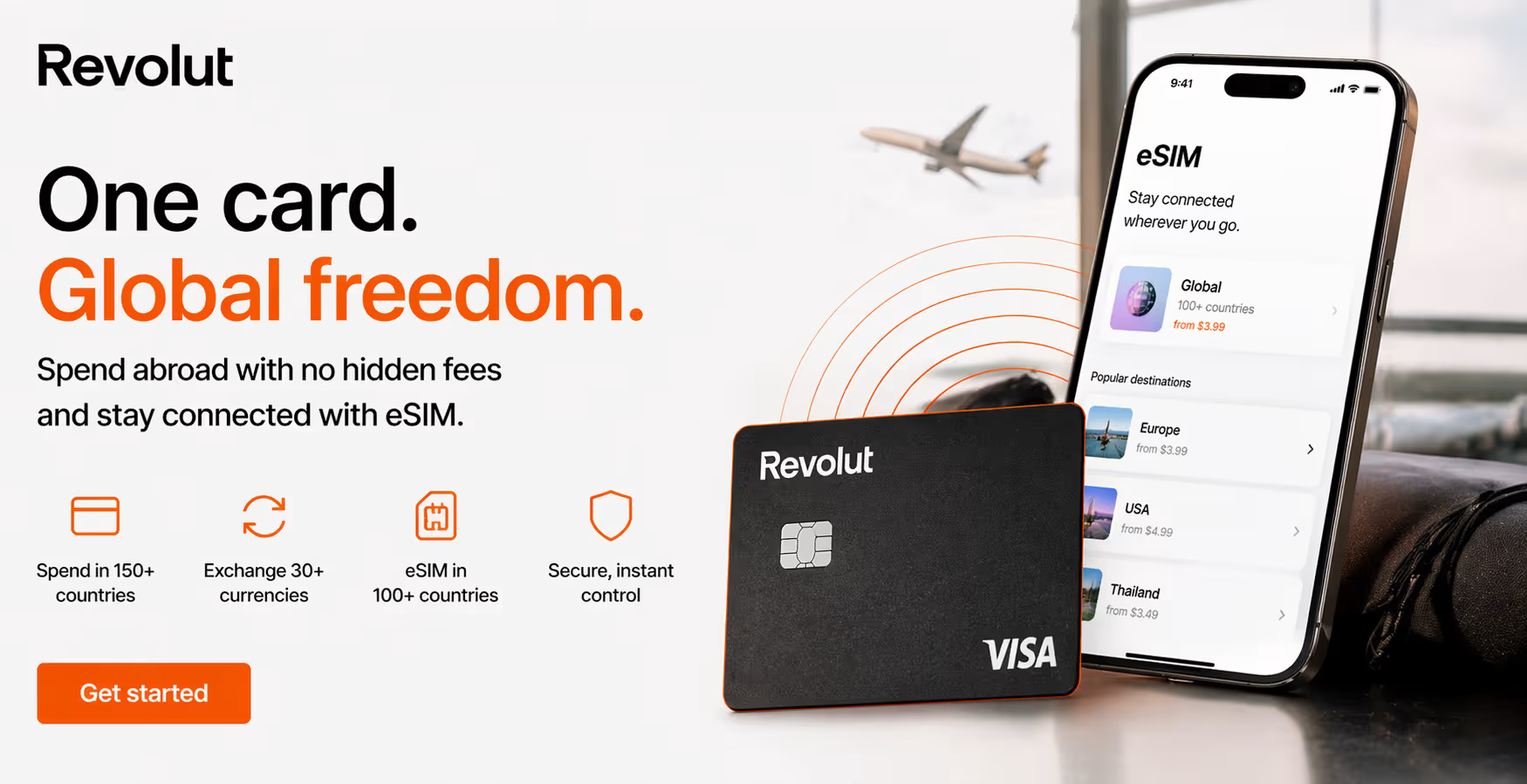

Revolut

Revolut is one of the strongest mobile payment apps for frequent travellers because it combines payments, cards, currency exchange, transfers, budgeting and travel-friendly controls in one place.

Revolut says users can send money to 160+ countries, receive payments from abroad and exchange 36 currencies through its international money transfer app. It also claims more than 70 million global customers. For travellers, that combination is hard to ignore.

Its biggest strength is control. You can create virtual cards, freeze cards, monitor spending quickly and move between currencies with more flexibility than a traditional bank app usually offers. The catch is that pricing depends on plan, usage, timing and country. Weekend exchange markups, fair usage limits and premium plan benefits all matter. Revolut is excellent, but it rewards users who actually read the details.

Wise

Wise is probably the most practical app for people who care about exchange rates and international spending. It is not trying to be a lifestyle super-app. Its core message is simple: hold, send and spend money across currencies with transparent pricing.

Wise says its card lets users pay online and in stores in over 40 currencies and 160 countries and territories, with support for Apple Pay and Google Pay. That makes it especially useful for business travellers, freelancers, digital nomads and anyone regularly crossing currency zones.

Wise feels built for people who actually move money across borders, not just people who occasionally buy a cappuccino abroad. It is especially useful for digital nomads, freelancers, business travellers and anyone annoyed by unclear bank conversion fees.

Wise is not always the flashiest app, but that is part of the appeal. It feels built for people who actually move money across borders, not just people who occasionally buy a cappuccino abroad. For Alertify readers, this is an important distinction. Travel payments are not only about convenience. They are also about avoiding quiet financial leakage from bad exchange rates, hidden fees and clumsy card controls.

Venmo, Cash App and local champions

Some payment apps are huge, but only in the markets where they truly belong. Venmo and Cash App are good examples in the United States. They are excellent for peer-to-peer payments, splitting bills, paying friends and handling casual money movement, but they are not universal travel wallets in the same way Apple Pay, Google Wallet, PayPal, Revolut or Wise can be.

Then there are local champions. WeChat Pay and Alipay dominate much of everyday digital payment behaviour in China. In India, UPI-based apps such as PhonePe, Google Pay and Paytm have changed the way people pay at scale. In parts of Europe, bank-connected apps and domestic wallet schemes remain important. In Africa, mobile money platforms such as M-Pesa show that “mobile payments” can mean something far bigger than card replacement.

This is where many global rankings get it wrong. There is no single best mobile payment app for every traveller, because payment behaviour is deeply local. A perfect app in London may be useless in Shanghai. A brilliant domestic wallet may not help much at a hotel desk in Paris. The best setup is usually a layered one.

What should travellers actually use?

For most international travellers, the smart approach is not to choose one app. It is building a small payment stack.

Use Apple Pay or Google Wallet for fast in-store and transport payments. Add PayPal for online purchases where buyer confidence matters. Use Revolut or Wise for currency management, international transfers and better control over cross-border spending. Then, depending on the destination, check whether a local wallet is essential.

China is the obvious example. A traveller who arrives expecting everything to work with a normal foreign card may quickly discover that local QR payment behaviour is far more important than card acceptance in many everyday situations. The same logic applies elsewhere, just in different forms. In some countries, QR payments dominate. In others, contactless cards are king. In others, cash stubbornly survives.

The hidden lesson is simple: payments are becoming destination infrastructure. Just like mobile data, roaming, maps and ride-hailing, the right payment app changes depending on where you land.

Final take

The best mobile payment apps are not winning because they are “apps.” They are winning because they sit close to moments of trust.

Apple Pay and Google Wallet own the device-native payment moment. PayPal owns much of the online trust moment. Revolut and Wise own the cross-border money movement. Local apps own the domestic behaviour moment. None of them solves the whole problem alone.

For travel brands, airlines, hotels, OTAs and even eSIM providers, this is worth watching closely. The payment layer is becoming part of the travel experience, not an afterthought at checkout. A traveller who can buy connectivity, pay for transport, check into a hotel and manage currency from the same phone has a smoother journey. A traveller who cannot pay cannot move.

That is why mobile payments should not be treated as a fintech side story. They are now part of travel technology infrastructure. And the next competitive edge may not come from who has the cheapest card fee or the nicest app screen. It may come from who understand the full journey: landing, connecting, paying, moving and staying in control.

Driven by wanderlust and a passion for tech, Sandra is the creative force behind Alertify. Love for exploration and discovery is what sparked the idea for Alertify, a product that likely combines Sandra’s technological expertise with the desire to simplify or enhance travel experiences in some way.