Monzo Launches UK Phone Plan That Gets Cheaper Each Year

Monzo is no longer just looking after your money. It now wants a place on your phone bill too.

The UK digital bank has opened a waiting list for Monzo Mobile, an eSIM-only phone plan built on the Virgin Media O2 network and expected to roll out this summer. The pitch is very Monzo: simple pricing, app-based control, no long contract, no exit fee, and a bill that gets cheaper the longer you stay.

There are three plans at launch: 10GB for £8 a month, 30GB for £12 a month, and unlimited data for £20 a month. All include unlimited UK calls and texts, 5G, WiFi calling, visual voicemail, hotspot use, and plan management inside the Monzo app. Customers also get 5% off their monthly bill each year, up to a maximum 30% discount.

Monzo is not trying to look like a traditional mobile operator. It is trying to make connectivity feel like another everyday financial product, sitting next to budgeting, payments, subscriptions, and travel spending.

Why banks want your SIM

Monzo is joining a wave of fintech brands moving into mobile connectivity because the customer relationship is shifting.

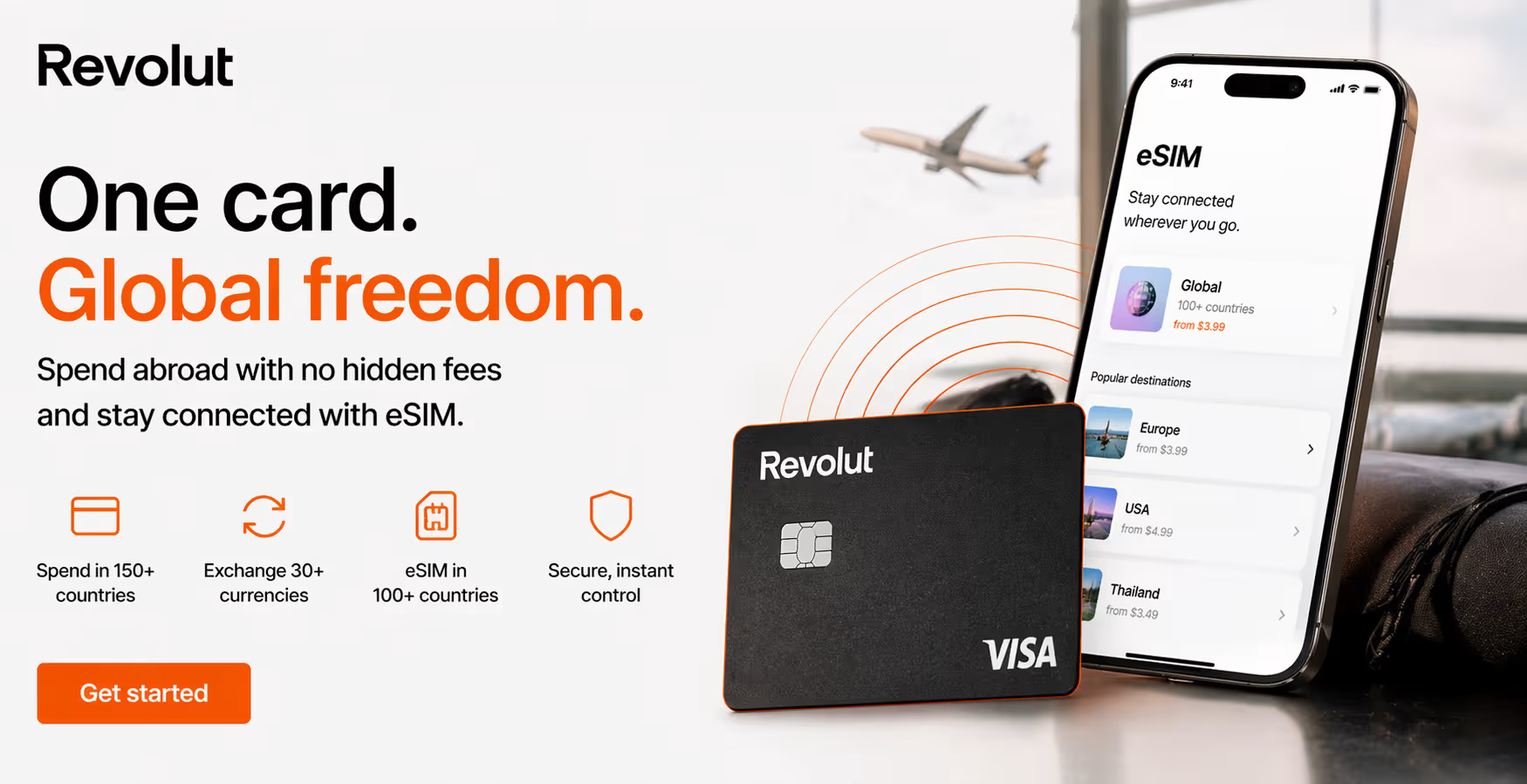

Revolut has already moved into UK mobile plans, offering unlimited 5G, calls and texts for £12.50 a month during its introductory period, with roaming included for the EU and US. These companies understand something many operators still underplay: customers increasingly trust apps, not networks.

That is where fintechs have an advantage. They already sit in the app layer. Monzo says it has more than 15 million customers, which gives it a huge base to test whether mobile can become another loyalty layer inside the bank.

The loyalty angle

The loyalty angle

The loyalty angle

The loyalty angleMonzo’s promise responds to one of the UK mobile market’s most unpopular habits: rewarding new customers while nudging loyal ones into worse value over time.

Since January 2025, Ofcom has banned inflation-linked and percentage-based mid-contract price rises in new phone, broadband and pay-TV contracts. Providers must now set out any price rises clearly in pounds and pence before the customer signs. That improves transparency, but it has not removed frustration around rising bills.

READ MORE: eSIM Revenue Models for Airlines, Banks and OTAs

Monzo flips the emotional message. Instead of “stay and pay more,” it says “stay and pay less.” Jez Samuel, mobiles expert at Uswitch, put it neatly: Monzo “isn’t breaking new ground” with the loyalty discount but that “broader adoption is a positive sign”.

He also added the important caveat:

“We’re seeing more players enter mobile than ever before, which can only mean more choice for consumers. Flexible, no-contract plans are appealing, but that flexibility cuts both ways as Monzo can change the price of its plans at any time.”

That last sentence matters. No contract and no exit fee are attractive, but they do not mean the price is permanently fixed. A flexible plan protects the customer from being trapped, not from future repricing.

The practical catch

Monzo Mobile will make the most sense for existing Monzo users who want simple in-app management and are comfortable with eSIM. It is less compelling for people who want the absolute cheapest UK SIM-only deal, a physical SIM, heavy EU roaming on the lowest plan, or a plan that is not tied to a current account relationship.

READ MORE: How Neobanks Are Disrupting the eSIM Market

The clearest improvement would be stronger roaming differentiation. Monzo’s 30GB and unlimited plans include 10GB of EU roaming, while the entry plan relies on low-cost roaming add-ons for more than 100 countries. For a digital bank with a travel-savvy user base, roaming could become the feature that makes the plan feel genuinely different.

There is also a communication challenge. “Unlimited” is one of the most abused words in mobile. Monzo will need to be clear about fair use, network management, speed expectations, roaming limits, and what happens if customers switch plans.

Alternatives worth considering

Revolut Mobile is the obvious comparison because it also wraps mobile connectivity inside a fintech app. Its single-plan approach is simpler, and the included EU and US roaming gives it a travel angle that frequent flyers will notice.

Traditional MVNOs such as Giffgaff, Lebara, Smarty and Tesco Mobile remain relevant too, especially for users who care mainly about price, coverage, or physical SIM flexibility. And the four UK network owners, EE, Virgin Media O2, Vodafone and Three, still control the infrastructure these challengers depend on.

The real takeaway

Monzo Mobile is not important because it offers an eSIM. It is important because it shows where consumer mobile is heading: away from telecom as a standalone purchase and toward connectivity as a feature inside larger digital relationships.

Banks, travel apps, airlines, retailers, and marketplaces are all learning the same lesson. If you already own the customer interface, selling connectivity becomes a natural extension. The battle is no longer only about who owns the mast. It is about who owns the moment when the customer thinks, “I need data, I need roaming, and I want this sorted now.”

For Monzo, the risk is that mobile becomes just another perk. The opportunity is bigger: making the phone plan feel as easy to manage as a bank card. If it can do that, the real pressure will be on legacy mobile providers that still make loyalty feel like a penalty.