Banks That Ignore eSIM Will Depend on Someone Else’s Network

Banks have spent years trying to become the centre of the customer’s financial life. Payments, cards, savings, insurance, travel perks, FX, budgeting, loyalty, subscriptions. The app is no longer just where people check their balance. It is where they manage their daily life.

So here is the uncomfortable question: if a customer lands in another country and cannot get online, how useful is that banking app?

That moment matters more than many banks realise. The traveller has just arrived. They need maps, hotel details, ride-hailing, WhatsApp, card verification, payment approval, and sometimes a bank security check. The bank may technically be ready to help. But without mobile data, it is standing behind a locked door.

This is why eSIM is becoming more than a travel add-on. It is quietly becoming part of the financial services experience.

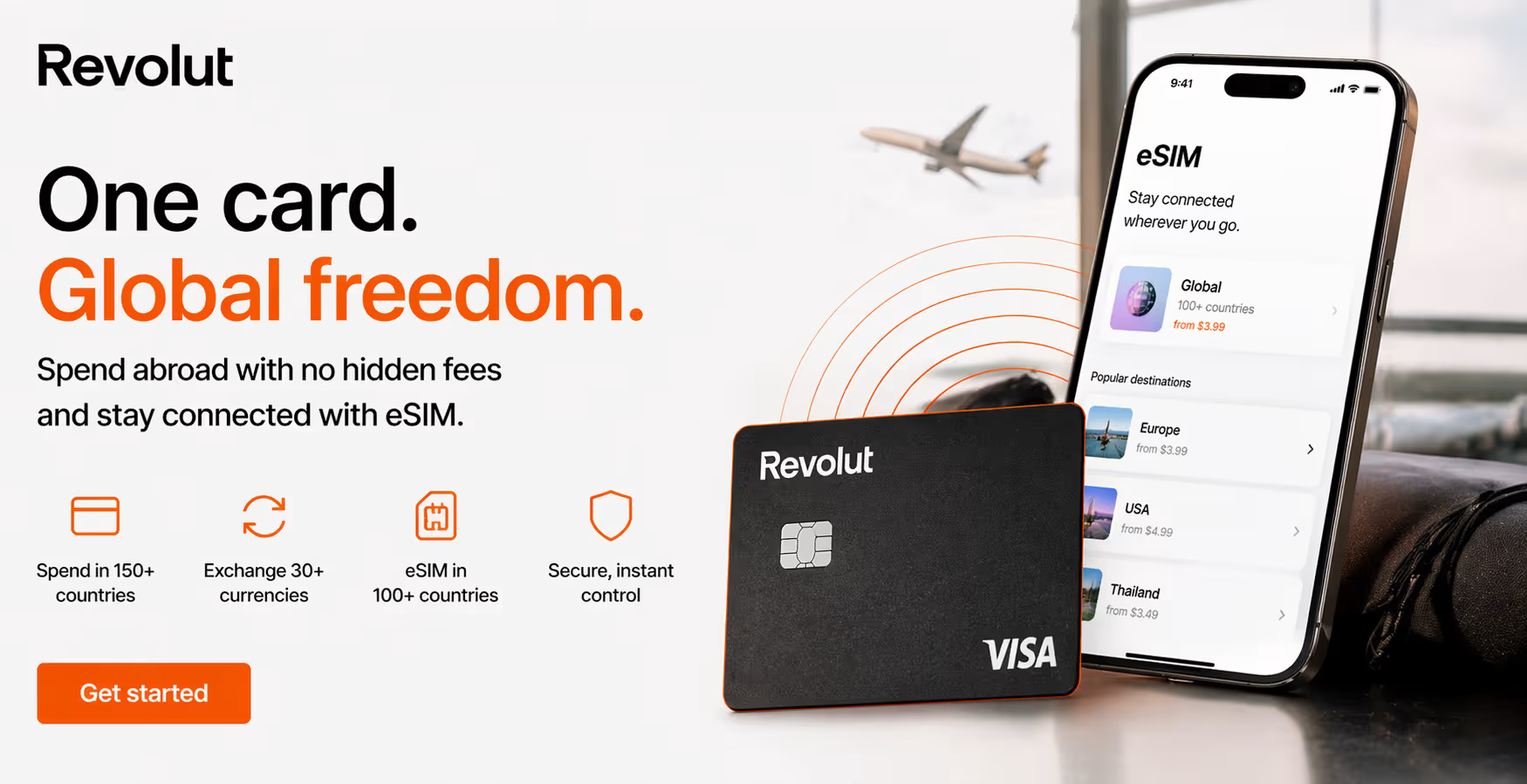

Revolut saw the gap early

Revolut is the obvious example. Its eSIM offer sits directly inside the app, with global data access in 100+ countries for Ultra users and paid data options for other customers. The point is not only the data plan. The point is the placement. Revolut does not send users into a separate telecom journey. It lets them manage connectivity in the same environment where they already manage money, cards, currency exchange, and travel benefits.

That is the signal banks should pay attention to.

The eSIM is not just another perk next to airport lounge access or travel insurance. It solves a practical problem at the exact moment the customer is most dependent on the bank app. When someone is abroad, connectivity is not a luxury. It is the layer that makes every other digital service usable.

And if a bank does not provide that layer, someone else will.

The network behind the relationship

For years, banks have been obsessed with owning the customer relationship. That made sense. Whoever controls the interface controls the habit. But travel connectivity adds a new twist: whoever controls the network can influence whether that relationship works at all.

A traveller with no data may not open the bank app. They may buy an eSIM from a travel eSIM provider, use a telco roaming bundle, or pick up a plan through another fintech, airline, hotel app, or super-app. The bank then becomes one of many services sitting on someone else’s connectivity layer.

That is not fatal. Banks do not need to become mobile operators. Most should not. But they do need to understand that connectivity is becoming a strategic dependency.

READ MORE: eSIM for Banks: Control the Experience or Lose It

The smarter approach is an embedded partnership. Platforms like Gigs now pitch phone plans and global eSIMs directly to fintechs as a way to increase revenue, loyalty, and app engagement. 1GLOBAL has also framed Telco-as-a-Service as a way for fintech and travel brands to embed mobile services without building telecom infrastructure from scratch.

In plain English: banks can offer connectivity without becoming telcos. But they still need the right partner, the right commercial model, and a user experience that does not feel bolted on.

Why is this not just about extra revenue?

Yes, eSIM can create a new revenue stream. That is attractive, especially for banks and fintechs fighting for subscription value and higher ARPU. But the bigger benefit may be retention.

A bank that helps customers avoid roaming shock earns trust in a very specific emotional moment. The customer is in a new country, slightly tired, probably looking for transport, and trying not to spend €50 on accidental roaming. Solve that problem and the bank stops feeling like a card provider. It starts feeling like a travel companion.

READ MORE: eSIM Technology and Fintech: Convenience or Control?

Giesecke+Devrient recently described eSIM packages as a way for fintechs and neobanks to deepen app ecosystems and create new value for users with global lifestyles. That is exactly the direction the market is moving in. Financial apps are no longer competing only on exchange rates or metal cards. They are competing on usefulness.

And usefulness abroad starts with being connected.

Your customers will buy connectivity. The question is: from you, or from someone else?

We help airlines, banks, and travel platforms turn that demand into a built-in product — not a missed opportunity.

The danger of choosing the wrong partner

This is where banks need to be careful. eSIM looks simple from the outside. Add a button, sell some data, make customers happy. But behind that button sit coverage agreements, network quality, data routing, refunds, fair usage rules, activation flows, customer support, compliance, and pricing logic.

A weak eSIM experience can damage the bank more than the telecom partner. Customers rarely care who powers the service in the background. If the plan fails, the bank app gets blamed.

READ MORE: Beyond Roaming Charges: How eSIM Unlock Global Connectivity for Fintech Users

That is why partner selection matters. Banks should not only ask, “Who gives us the cheapest data?” They should ask: Who has reliable coverage in our customers’ most common travel corridors? How transparent are the terms? What happens when activation fails at midnight in another time zone? Can the partner support our brand standards? Can they scale across markets? Can we integrate without creating a clumsy user journey?

This is also where specialist market knowledge helps. Alertify, for example, sits close to the travel eSIM, roaming, telecom, and embedded connectivity ecosystem, which makes it easier to understand which partners are built for consumer travel, which are stronger in B2B infrastructure, and which models actually fit a bank’s audience. The best partner is not always the loudest provider. It is the one whose network, support, pricing, and product logic match the bank’s customer promise.

Conclusion

Banks do not need to rush into eSIM because it is trendy. They need to look at it because the banking experience is becoming dependent on connectivity.

The winners will not be the banks that simply add a travel data tile and call it innovation. The winners will be the ones who understand the deeper shift: money, identity, travel, security, and connectivity are starting to sit inside the same customer journey.

Ignore eSIM, and banks will still operate abroad. But they will do it on someone else’s network, inside someone else’s customer moment, and possibly after someone else has already solved the traveller’s first real problem.

That is the opportunity. Not telecom for the sake of telecom. Connectivity is the missing layer of modern banking.