Why Some Crypto Purchases Require Verification and Others Do Not

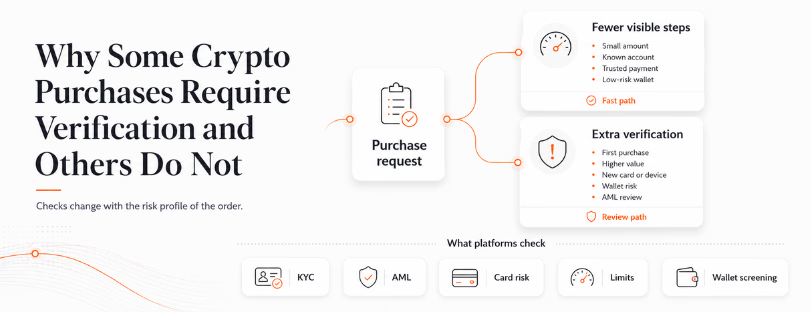

Crypto purchases do not all follow the same identity process because order size, payment method, location, account history, wallet risk, and provider policy affect the review. A small repeat purchase from a known account is different from a first card payment, a high-value order, or a transaction linked to a higher-risk wallet.

A buyer comparing crypto exchange services such as switchere.com sees verification as part of the purchase flow, while the provider reviews identity data, payment approval, fraud signals, sanctions screening, transaction limits, and wallet information. Some purchases need fewer visible steps because earlier account checks already created enough evidence, while other orders trigger extra review because the risk profile is higher.

Checks That Decide the Purchase Flow

A crypto platform separates orders into different review paths before assets are released. The main factors include KYC rules, AML controls, card payment exposure, transaction tiers, and failed verification signals.

KYC Rules

Know Your Customer checks confirm that the person behind the account matches the details provided during registration or purchase. A platform checks name, date of birth, address, document images, selfie match, device data, and account history. The purpose is to connect the transaction to a real user and reduce identity misuse.

Verification level depends on the provider’s risk model and legal environment. A lower-tier account has smaller purchase limits and fewer approved payment options. A higher-tier account requires more information, stronger document review, and extra checks before larger orders move through the system.

A KYC review focuses on identity facts that support account ownership:

- Personal details that match the submitted identity document.

- A live selfie or face check linked to the document image.

- Address, region, and account data that match platform requirements.

KYC checks whether the platform has enough identity evidence to process the order under its rules. That distinction matters because verification is about access control and risk, not price direction.

AML Checks

Anti-money laundering checks look at transaction behavior, sanctions exposure, account patterns, and risk indicators. Virtual asset service providers are expected to apply AML and counter-terrorist financing controls under international standards, while national regulators apply local versions of those rules. This is why a platform screens both customer data and transaction activity.

AML systems review patterns across time. A single purchase has one risk profile, while repeated orders, rapid limit changes, mismatched locations, or unusual wallet activity create another. Extra checks are added when the platform needs more evidence about the user, funds, or destination.

AML review uses several signals before an order is completed:

- Sanctions and politically exposed person screening.

- Repeated purchase attempts across cards, accounts, or devices.

- Sudden increases in order size after low activity.

- Wallet risk data from blockchain analytics tools.

- Source-of-funds information for higher-value activity.

AML controls explain why two users see different steps for the same asset. One account has a clean history and a lower amount, while another has a new device, a larger order, and a wallet linked to risky activity.

Card Payment Risk

Card purchases create a different risk from bank transfers or existing account balances. The payment processor checks card number, expiry date, CVV, billing information, 3D Secure result, issuer response, device signals, and fraud score. Approval from the issuer confirms payment authorization, but it does not remove dispute risk for the merchant.

Crypto delivery creates a timing mismatch for providers. A blockchain transfer is difficult to reverse after completion, while card payments remain subject to disputes and chargeback processes. This is why platforms add fraud review before releasing assets to a wallet.

Transaction Limits

Transaction limits are tied to verification tiers. A new account starts with smaller limits because the platform has less history and less identity evidence. Higher limits require stronger verification, longer account history, document checks, and sometimes source-of-funds information.

Limits are also used to manage operational risk. A provider watches order size, purchase frequency, card use, failed attempts, country data, and wallet destination. A user who stays within a low tier sees fewer requests than someone who raises volume quickly or changes payment details.

Failed Verification

Verification fails when the platform cannot match the user, document, payment method, region, or wallet to an acceptable risk profile. Common causes include expired documents, poor image quality, mismatched names, blocked regions, failed selfie checks, unsupported cards, suspicious wallet data, or inconsistent account information.

A failed check means the platform lacks enough evidence to approve the order under its rules. Clear status messages help users understand whether the issue relates to identity, payment, document quality, or destination address.

Why Verification Paths Differ

Verification requirements differ because crypto purchases combine payment risk, identity control, wallet risk, transaction size, and regional compliance in one flow. A low-value order from a verified account has a different review path from a first card purchase, a larger order, or a transfer to a higher-risk wallet. The user sees either a short checkout or extra document requests, but the platform is matching the purchase to the level of evidence needed before asset delivery.