United Group Builds Key Greece–Balkans Fiber Route

Something important just happened in the Balkan telecom space and, like most infrastructure moves, it flew under the radar. United Group has completed a 600 km terrestrial fiber cable linking Athens and Thessaloniki. On paper, that sounds like a domestic upgrade inside Greece. In reality, it is much bigger than that. B

alkan fiber backbone connectivity

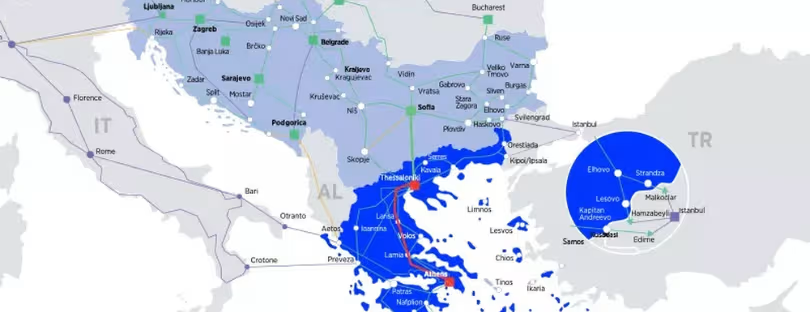

This route, built by United Fiber, is now part of a growing regional backbone that stretches far beyond Greek borders. It connects eight major cities along the way and plugs directly into United Group’s wider network across Southeast Europe, running through Sofia and into Western Europe.

If you look at the map, what they’ve done is strengthen one of the most strategic corridors in the region.

And right now, that matters more than ever.

Why this route actually matters

At first glance, Greece already has strong international connectivity through submarine cables to Italy and other Mediterranean hubs. So why invest heavily in a terrestrial route?

Because redundancy and control are becoming critical.

The new cable connects Athens, Thessaloniki, Volos, Lamia, Larissa, Livadeia, Katerini, and Thebes, forming a high-capacity inland route that complements existing submarine infrastructure. That means traffic doesn’t rely on a single path anymore.

And in today’s environment, that is not a technical detail. It is a strategic decision.

With growing geopolitical sensitivity around data flows and increasing reliance on cloud services, operators want diversified, resilient routes. A strong terrestrial backbone reduces dependency on undersea cables, which are more vulnerable to disruptions, whether accidental or intentional.

This is exactly the kind of infrastructure layer most users never see, but everything depends on it.

From Greece to a regional corridor

What makes this project interesting is not just the Greek footprint, but how it connects outward.

Once traffic reaches Thessaloniki, it moves north through Sofia and into United Group’s broader Balkan network. From there, it links into Western Europe.

At the same time, the southern end connects into existing and planned routes toward Turkey and the Middle East.

This positions Greece as more than just a coastal landing point. It becomes a transit hub between:

- Western Europe

- The Balkans

- Turkey

- The Middle East

That shift is already underway. Greece has been investing heavily in data centers and international connectivity, with players like Microsoft and Digital Realty establishing infrastructure in the region.

This new cable fits directly into that trend.

The wholesale angle most people miss

Another important layer here is UGI Wholesale, the unit responsible for commercializing the network.

They are not just building infrastructure for internal use. They are actively selling capacity to carriers, tech companies, and service providers.

That includes:

Data transport

High-capacity routes for cloud providers and hyperscalers

Voice and mobile services

Support for cross-border telecom operations

Roaming infrastructure

Critical for mobile connectivity across Europe and beyond

This matters because the real value of these networks is unlocked through wholesale access. Infrastructure becomes a platform, not just a pipe.

And demand is rising fast.

According to TeleGeography and GSMA Intelligence, international bandwidth demand continues to grow at double-digit rates, driven by cloud computing, video traffic, and enterprise digitalization. The Balkans and Southeast Europe are no exception.

Competing in a crowded infrastructure race

United Group is not alone in this space.

Across Europe and neighboring regions, several players are investing heavily in similar corridors:

- A1 Telekom Austria Group is expanding fiber and mobile infrastructure across Central and Eastern Europe

- Deutsche Telekom continues to strengthen cross-border backbone networks

- Telecom Italia Sparkle is positioning itself as a major Mediterranean connectivity hub

- OTE (Cosmote) in Greece is also investing in both terrestrial and submarine capacity

And then there are global infrastructure players and submarine cable consortia building new routes between Europe, Asia, and Africa.

So, where does United Group stand?

Their advantage is regional depth.

While larger incumbents focus on pan-European or global scale, United Group is building a dense, integrated network specifically across Southeast Europe. That gives them stronger control over routes in a region that has historically been fragmented.

This is a different kind of strategy. Less about global dominance, more about regional ownership.

The bigger trend: infrastructure is shifting east and south

Zoom out for a second, and a clear pattern emerges.

Connectivity is no longer centered only around traditional Western European hubs like Frankfurt, Amsterdam, and Paris.

Instead, new corridors are forming:

- Mediterranean routes linking Europe to Africa and the Middle East

- Balkan corridors connecting Central Europe with Turkey and beyond

- Southern European hubs gaining relevance due to latency advantages and diversification needs

Greece, in particular, is becoming a key node in this new map.

Projects like this terrestrial cable, combined with planned submarine links across the Aegean, are turning the country into a connectivity bridge between continents.

This is supported by broader industry data. TeleGeography’s Global Bandwidth Research shows strong growth in inter-regional capacity between Europe and Asia, while EU-backed initiatives continue to push for digital infrastructure resilience across member states.

In other words, this is not an isolated investment. It is part of a structural shift.

What this means for the market

For enterprises, cloud providers, and even travel connectivity players, this kind of infrastructure quietly changes the playing field.

Better routing options mean:

- Lower latency across regions

- More stable connectivity for international services

- Increased competition among carriers

- Potential cost optimization in the long run

For the eSIM and roaming ecosystem, which relies heavily on wholesale agreements and underlying network quality, these upgrades matter more than they might seem.

The quality of your “global data plan” ultimately depends on infrastructure like this.

Conclusion: not just another cable

This is where it gets interesting.

United Group is not trying to outbuild global giants. They are doing something more focused.

They are locking down a region that is becoming increasingly important in global connectivity flows.

Compared to players like Deutsche Telekom or Telecom Italia Sparkle, their scale is smaller. But their positioning is sharper. They are building density and control in Southeast Europe at a time when that region is gaining strategic importance.

And that aligns with a broader industry shift.

Infrastructure is no longer just about capacity. It is about geography, resilience, and control over routes.

Projects like this, the Athens to Thessaloniki cable, are part of a larger rebalancing of the network map, where Southeast Europe moves from the edge to a central transit role.

If that trend continues, the real winners will not just be the biggest operators, but the ones who own the right corridors at the right time.