How to Apply for a Revolut Card (Fast & Simple Guide)

If you’re still thinking about “applying” for a card the old-school way, forms, waiting rooms, paperwork… you’re already behind.

With Revolut, getting a card is closer to setting up an app than dealing with a bank. And that shift says a lot about where financial services are going, especially for travelers and digitally native users.

Let’s break it down properly, not just how to apply, but what you’re actually signing up for.

It starts with the app, not the bank

There’s no branch visit. No awkward meeting with an advisor. Everything begins with downloading the Revolut app.

From there, the process is surprisingly lean:

- Sign up with your phone number and email

- Enter basic personal details

- Verify your identity (passport or ID + selfie)

- Add some money

- Order your card

That’s it. In most cases, you’ll have a virtual card ready almost instantly, even before the physical one arrives.

It’s not just fast, it’s deliberately frictionless. That’s the point.

What you actually need (and what you don’t)

Here’s where things get interesting. The “requirements” are minimal compared to traditional banking, but they’re still strict where it matters.

You’ll need

- ✓ Government-issued ID, such as a passport or driving licence

- ✓ A valid phone number and email address

- ✓ Proof of residency in a supported country

- ✓ Basic personal details and a selfie for verification

You don’t need

- — A credit history for debit or prepaid cards

- — A minimum deposit to open the account

- — Any in-person verification

Most users can get through onboarding in minutes, not days.

That’s a huge shift if you’ve ever opened a traditional bank account.

Virtual vs physical card (and why it matters)

This is where Revolut quietly changes user behavior.

You don’t just “apply for a card.” You choose how you want to exist financially:

Virtual cards

- ✓ Instant creation

- ✓ Perfect for online payments

- ✓ Can be single-use (auto-refresh for security)

Physical cards

- — Needed for ATMs and some real-world payments

- — Delivered after ordering

- — Often free (you just pay delivery on basic plans)

Most users start spending with the virtual card immediately while waiting for the physical one.

That instant usability is one of Revolut’s strongest hooks.

The hidden layer: it’s not just a card

Here’s where many people misunderstand Revolut.

You’re not applying for a “card” in the traditional sense. You’re opening a multi-currency financial layer with a card attached to it.

That includes:

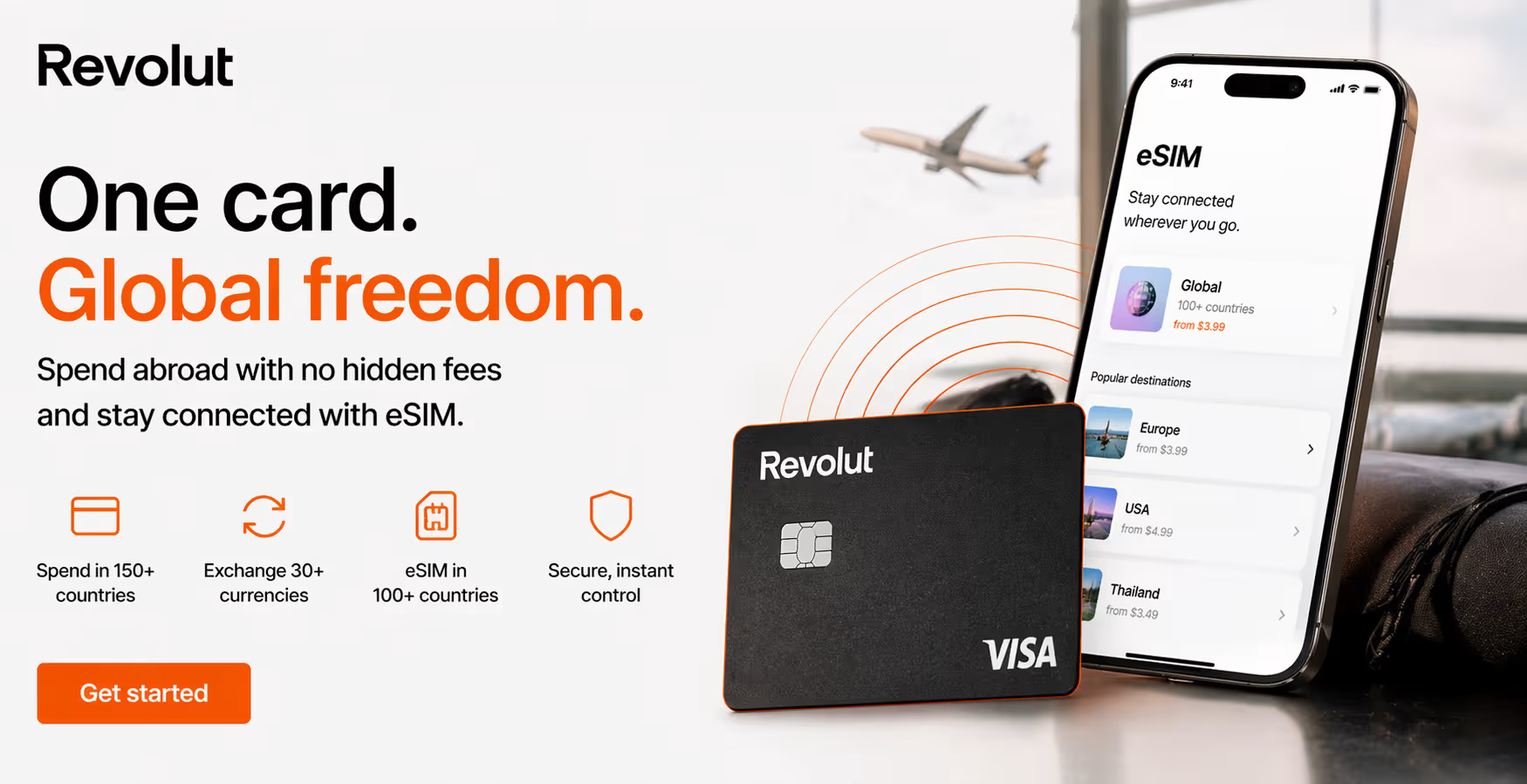

- Spending in 150+ currencies

- Real-time expense tracking

- In-app currency exchange

- Card-level security controls (freeze/unfreeze instantly)

In other words, the card is just the interface. The product is the system behind it.

And for travelers, that distinction matters.

Credit cards are a different story

Now, if you’re specifically looking to apply for a Revolut credit card, things get more fragmented.

Unlike the debit/prepaid card:

- Availability depends on your country

- You’ll need income verification and credit checks

- Approval isn’t guaranteed

In some markets, you can apply directly in-app and get a decision quickly, sometimes within minutes.

But in others, the product simply isn’t available yet.

That inconsistency is one of Revolut’s current limitations.

Why travelers are switching (and what they don’t tell you)

From a travel tech perspective, this is where Revolut becomes more than just convenient.

Applying for a Revolut card effectively gives you:

- A low-friction way to spend abroad

- Better FX rates than many traditional banks

- Immediate visibility on what you’re spending

That’s why it keeps showing up in “best travel card” conversations.

But there’s a nuance most guides skip:

Revolut is not a full replacement for everything.

For example:

- Car rentals often still require a credit card deposit

- Some edge cases (hotels, offline terminals) prefer traditional cards

- ATM limits and fees vary depending on your plan

Even Revolut itself acknowledges that a backup card is still a smart move.

Where this fits in the bigger fintech shift

Applying for a Revolut card is less about getting plastic and more about joining a new model of banking.

Compare that to players like:

- Wise — stronger on international transfers and transparent FX

- N26 — more “bank-like” experience in Europe

- Monzo — focused on budgeting and domestic banking

Revolut sits somewhere in between:

- More feature-heavy than most

- More global than many neobanks

- Slightly less focused than specialists like Wise

And that’s both its strength and its weakness.

Conclusion

Applying for a Revolut card is almost deceptively simple. A few taps, a quick identity check, and you’re in.

But what you’re really doing is opting into a different financial model. One that prioritizes speed, control, and global usability over traditional banking structure.

That model works incredibly well if:

- You travel frequently

- You manage multiple currencies

- You value real-time control over your spending

It’s less perfect if:

- You need full credit infrastructure everywhere

- You rely on traditional banking protections and services

The bigger trend is clear though. Fintech isn’t trying to replicate banks anymore. It’s replacing specific parts of them, piece by piece.

And the “apply for a card” moment is where most users first feel that shift.

Not because it’s complicated.

Because it’s suddenly… not.