eSIM & iSIM Set to Hit 4.4 Billion Connections by 2028

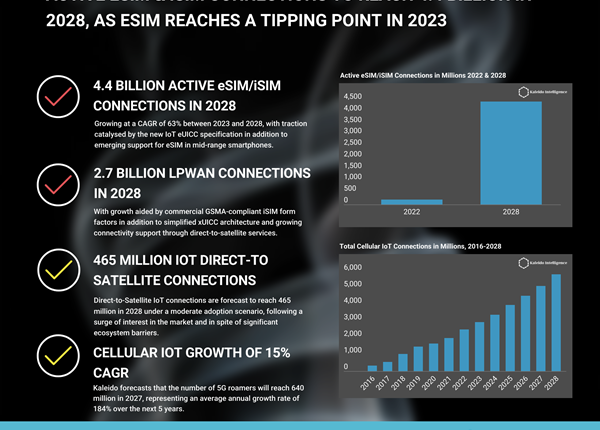

The numbers are striking, but the story behind them is more interesting. Kaleido Intelligence has forecast that total active xUICC connections — that’s eSIM and iSIM combined — will approach 4.5 billion by 2028, representing a 63% CAGR from 2023. It’s a headline-worthy figure, but what it really signals is a structural shift that’s been building for years and is now impossible to ignore.

This isn’t hype. It’s infrastructure.

What Slowed the Market — and Why That’s Behind Us

The path to that 4.5 billion figure wasn’t straight. Supply chain disruptions from COVID-19, the chipset shortage, and the knock-on effects of the war in Ukraine all pushed back expected mid-range smartphone launches with eSIM support. For a technology that depends heavily on installed base, delayed hardware rollout matters — it compresses the market window for operators, MVNOs, and the travel eSIM layer on top.

Despite that, activation rates held up. Both consumer and IoT segments showed real traction, and the majority of operators moved to support eSIM onboarding during this period. The infrastructure was built quietly under pressure.

Now the headwinds are clearing. Mid-range smartphones — where the real volume lives — are finally coming to market with eSIM support. Global eSIM penetration in smartphones stood at 28.9% in 2024 and is expected to grow to 57.7% by 2030, but the more immediate lever is the sheer scale of mid-range rollouts that are now underway. Premium devices proved the concept. Volume devices will drive the numbers.

SGP.32: The Specification That Changes IoT Economics

If mid-range smartphones are the consumer catalyst, the SGP.32 specification is the IoT equivalent. The GSMA ratified SGP.32 in June 2024, and its implications for industrial deployments are significant. It borrows architecture from the consumer eSIM world and applies it to IoT devices — dramatically simplifying what was previously a fragmented, technically painful landscape built on the older M2M specification.

Kaleido’s Research Lead Steffen Sorrell put it plainly:

“2023 is expected to represent a tipping point for realising the original vision and value for eSIM, particularly in the IoT domain. In essence, eSIM as a long-term bet for IoT will become much more valuable, while the onboarding of eSIM in mid-range smartphones will dramatically increase the installed base for handsets while encouraging operators to refine their eSIM onboarding processes and eSIM connectivity strategies.”

The practical effect: a wider ecosystem of available profiles, reduced integration friction, and lower costs for multinational deployments. For IoT operators managing fleets across multiple markets, that’s not a marginal improvement — it’s a fundamentally different operating environment.

iSIM: The Quiet Contender

While eSIM gets most of the attention, iSIM is the technology to watch over the next three to five years. Juniper Research forecasts iSIM connections will reach 210 million by 2028, targeting use cases like smart energy meters and remote logistics — sectors where power efficiency and compact form factors are non-negotiable.

Qualcomm and Thales have already validated the first GSMA-certified iSIM on the Snapdragon 8 Gen 3. That’s a significant hardware milestone. Once iSIM is shipping at scale inside flagship silicon, the cost curves shift and adoption in adjacent categories accelerates. Counterpoint Research estimates iSIM shipments will grow at a 160% CAGR between 2024 and 2030, dwarfing eSIM’s already impressive trajectory.

The distinction matters for platform vendors and operators: iSIM devices don’t just have embedded SIMs, they have SIM functionality baked into the main processor. That changes security architecture, supply chain dynamics, and the competitive positioning of traditional SIM manufacturers.

LPWAN Connections: A Perfect Storm

Kaleido’s research also touches on LPWAN, and the framing of a “perfect storm” is accurate. Three forces are converging: SGP.32 simplifying IoT provisioning, iSIM lowering hardware costs and footprint, and direct-to-satellite connectivity reaching commercial viability. The GSMA predicts 6.9 billion eSIM connections by the end of 2030, and LPWAN is a meaningful contributor to that scale. Connections are projected to reach 2.7 billion in 2028 — connecting sensors, meters, and logistics nodes across geographies that traditional cellular infrastructure barely reaches.

This is where the real enterprise opportunity sits. Lower initial cost for multinational deployments, plus long-term flexibility to optimize connectivity providers over the air, is the pitch that unlocks large-scale industrial contracts.

The Travel eSIM Layer

For Alertify readers, there’s a direct line from these macro trends to the retail connectivity market. Kaleido Intelligence forecasts retail spending on travel eSIM services will hit $3.3 billion, almost 165% higher than the prior year, with 50% annual growth projected over the following four years. That would make travel eSIMs responsible for 28% of all travel connectivity retail spending by 2028.

The providers positioned to capture that are the ones building distribution and operational scale now — not just in 2026 or 2027. Holafly has built brand recognition through aggressive content and affiliate marketing. Airalo continues to dominate on breadth of coverage. Ubigi and Nomad compete on data pricing and plan flexibility for frequent travelers. Yesim and Airhub are carving out B2B and API-distribution angles. The consumer market is crowded, and differentiation is shifting from “does it work?” to “how seamless is the experience, and what’s the price-per-GB at destination X?”

What Actually Comes Next

The Kaleido forecast is compelling, but context matters. Kaleido, Juniper Research, ABI Research, and Counterpoint are all pointing in the same direction — high CAGR, multi-billion connection scale, IoT as the long-term volume driver. Where they differ is in timing and the relative weight of consumer vs. industrial growth. ABI Research recorded 490 million eSIM device shipments in 2024, with 544 million forecast for 2025 — solid, but incremental rather than exponential on the consumer side. The real inflection comes when mid-range Android devices in Southeast Asia, India, and Latin America fully normalize eSIM, and when SGP.32-enabled IoT deployments start shipping at industrial scale.

The platforms that will matter in 2028 aren’t necessarily the ones with the most profiles today. They’re the ones building standard-agnostic infrastructure — capable of handling SGP.22, SGP.32, and whatever comes next — while maintaining operator relationships across both consumer and M2M. That’s a different kind of company than a travel eSIM reseller, and the market is starting to make that distinction clearer. The 4.5 billion connection figure isn’t a destination. It’s a checkpoint.