The Post-Roaming Power List: Who Wins Next?

Roaming is not dead. That would be too simple and too convenient for telecom headlines.

But roaming is weaker than it used to be.

The old machine still works. Operators still have wholesale deals, steering systems, settlement processes and decades of muscle memory behind them. The uncomfortable part is different: roaming is no longer the only answer travelers understand.

For years, international connectivity was something customers accepted with a grim little shrug. You landed, turned on data, hoped your package covered the country, and waited for the bill. In Europe, regulation softened the problem. Elsewhere, bill shock remained a travel ritual. Then travel eSIMs arrived with a different promise: choose before you go, pay upfront, install digitally, connect on arrival.

The product is not perfect. Coverage varies. Support can be uneven. Unlimited plans need careful reading. Some apps look polished until activation fails in a taxi queue. But the direction is clear. Roaming is being pulled out of the operator-only world and pushed into apps, APIs, travel platforms, banks, device ecosystems and enterprise workflows.

GSMA Intelligence says eSIM smartphone penetration was about 5% at the end of 2025, with 10% expected by the end of 2026. Juniper Research estimated travel eSIM revenue at $1.8 billion in 2025 and forecast $8.7 billion by 2030. The European Commission has also extended “roam-like-at-home” rules until 2032, which keeps pressure on legacy roaming economics inside Europe.

So this is not a list of companies that “killed roaming.” Nobody did that. It is a power list of the companies and categories that benefit as traditional roaming loses its grip on the traveler relationship.

Travel eSIM brands

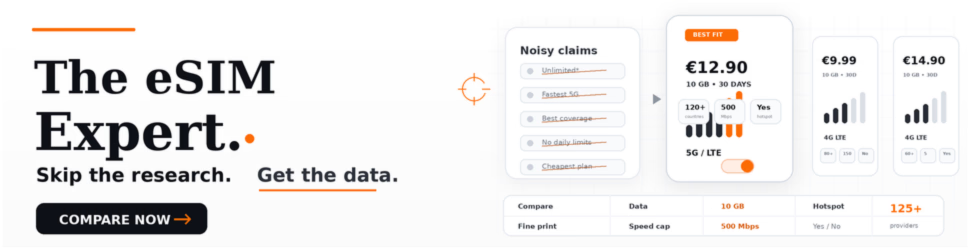

The first obvious winners are the travel eSIM specialists.

Airalo made the category feel normal for mainstream travelers. Holafly pushed a simpler unlimited-data story. Nomad eSIM built a clean app-first experience. Saily entered with a cybersecurity-adjacent brand. Ubigi has strength in connected cars and global data use cases. GigSky still has a position in cruise and airline partnerships. Yesim, Maya Mobile, Roamless, Numero eSIM, Telfoni and others show how wide the market has become.

This group benefits because it speaks the traveler’s language better than most mobile operators do. Not “retail roaming add-on.” Not “zone three pass.” Just “your phone works in Japan for this price.”

That sounds basic, but it is a serious advantage. Travel eSIM providers sell clarity. They make international mobile data look like a travel product, not a telecom contract. The best ones understand timing too. A traveler does not want to compare roaming tariffs at midnight before a flight. They want a plan, an app install, and confidence that it will work.

Where this group still needs to improve is reliability after the sale. A beautiful checkout is meaningless if the profile will not activate, the data route is slow, or support replies six hours later. As the market matures, the winner will not always be the cheapest provider. It will be the one that combines price, coverage transparency, refunds and fast human support.

Connectivity API platforms

The quieter winners sit behind the storefronts.

Connectivity API platforms let travel brands, fintechs, OTAs, loyalty apps and digital banks sell eSIMs without becoming telecom companies. This is where roaming really starts to lose structural power. The customer may think they are buying connectivity from an airline, bank or booking platform, but the operational layer is handled by an API provider, MVNE, MVNO, aggregator or embedded connectivity specialist.

Companies such as 1GLOBAL, Telna, Gigs, eSIM Go, Monty Mobile and other infrastructure players sit in this space. Some lean toward consumer distribution. Others are stronger in enterprise, IoT, MVNO enablement or branded connectivity. The common thread is simple: they turn telecom access into software.

That matters because software distribution scales faster than traditional roaming distribution. An airline can add connectivity to a booking flow. A bank can offer travel data inside a premium account. A corporate travel platform can add global data to employee mobility.

This is not for every brand. Selling connectivity brings support, refunds, failed activations and customer expectations. If a hotel group simply wants “extra revenue” without owning the customer experience, it may create more irritation than loyalty. But for platforms with strong travel intent, embedded eSIM is becoming one of the most natural add-ons in the market.

Airlines and travel platforms

Airlines benefit because they own one of the most valuable moments in travel: before departure.

That moment used to be monetized with baggage, seats, insurance, hotels, lounges and car rentals. Connectivity now belongs in the same conversation. A customer flying from London to Bangkok already expects the airline app to manage the trip. Adding mobile data is no longer strange. It feels overdue.

The same logic applies to OTAs, booking platforms, rail apps, cruise sellers, airport apps and destination marketplaces. These companies may never want to become eSIM brands. They do not need to. Their advantage is timing and context.

If a traveler books a trip to Turkey, Morocco, Japan or the United States, the platform already knows the destination, dates and likely connectivity need. That makes a generic roaming plan look clumsy. A smart embedded offer can be more relevant, cheaper and easier to understand.

The challenge is trust. Travel platforms are already full of add-ons, and customers have learned to skip anything that feels like a checkout trap. Connectivity cannot be sold like another insurance checkbox. It needs clear coverage, fair pricing and honest limitations.

Banks and device ecosystems

Banks and fintechs are underrated winners.

Their customers travel. Premium accounts already include insurance, lounge access, FX benefits, virtual cards, fraud alerts and subscriptions. Connectivity fits that bundle surprisingly well. It can be a perk, a paid add-on, a loyalty reward, or part of a business travel package.

The logic is not only convenience. It is identity and security. A traveler with mobile data can approve card payments, receive alerts, access banking apps, message support and use maps without gambIing on public Wi-Fi. That makes connectivity part of the financial travel experience.

This is where companies with local numbers, voice, SMS or identity-adjacent features may have a stronger story than pure data-only eSIM apps. Numero eSIM plays in the wider communication layer. Telfoni’s voice and telco background positioning also matters because banks tend to care about reliability, trust and continuity, not only price per gigabyte.

Device makers also gain. Apple’s eSIM-only iPhone move in the United States did not just remove a tray. It changed the mental model. When users understand multiple profiles, app-based activation and switching plans, the traditional operator loses some of its default advantage. Apple, Samsung, Google, and other ecosystem players benefit because eSIM makes phones more flexible and software-defined.

The risk is execution. Banks are not loved for telecom support. If they add eSIM badly, customers will blame the bank, not the invisible provider behind it. Partnerships and service design matter as much as the wholesale rate.

Operators that adapt

Operators that adapt

Operators that adapt

Operators that adaptNot every mobile operator loses.

The operators most exposed are those relying on expensive, confusing, passive roaming margins. The ones with strong travel products, wholesale networks, digital onboarding and partner distribution can still win.

Orange Travel is a useful example because it brings operator credibility into the travel eSIM category. Vodafone, Deutsche Telekom, Telefónica, Singtel, e&, T-Mobile and other large groups also have the scale, roaming relationships and network knowledge to compete if they package the offer properly. The problem is not capability. It is reflex.

Operators that adapt will stop treating travel eSIM as a defensive side product. They will use it as a new distribution layer: direct to consumers, through partners, through enterprise platforms, and through branded travel bundles.

Enterprise mobility

The post-roaming shift is not only about consumer travel.

Enterprises are also tired of uncontrolled roaming bills, messy reimbursements and employees buying random local SIMs or consumer eSIMs. Global workforce connectivity needs visibility, policy, procurement alignment and support. That is a different problem from “I need 5GB for Spain.”

This benefits enterprise eSIM providers, global MVNOs, mobility management platforms and managed connectivity specialists. Companies such as 1GLOBAL, Vodafone Business, Tata Communications, Gigs, Airalo for Business, Holafly Connect and other enterprise-focused providers are moving around this opportunity from different angles.

The strongest enterprise players will not simply sell cheaper data. They will sell control: who gets connectivity, where it works, how usage is tracked, how costs are allocated, and what happens when someone lands in a country not covered by the policy.

Consumer eSIM brands can move into business, but enterprise buyers are less patient with app-only support and unclear governance. The companies that understand procurement language have an edge.

Niche travel winners

Some of the most interesting post-roaming winners are in niche travel.

Cruise connectivity is a good example. For years, it was awkward, expensive and confusing. GigSky built early recognition in cruise eSIMs, and Maya Mobile has now entered with a global cruise eSIM plan that combines land and sea coverage. That signals a broader point: once eSIM becomes a flexible distribution layer, niche travel segments become commercially interesting.

The same applies to aviation, connected cars, rail corridors, maritime crews, digital nomads and cross-border workers. These are valuable because connectivity pain is high and standard roaming is often poorly suited.

Niche winners usually have one advantage over generic eSIM sellers: they understand the actual context. A cruise passenger does not have the same needs as a weekend city-break traveler. A connected car does not behave like a smartphone. A remote worker crossing borders every week needs continuity, not just a cheap promotional plan.

The companies at risk

The biggest losers are not “telcos.” That is too broad.

The losers are companies that depend on customer confusion, poor price visibility or captive distribution. If a customer only buys roaming because they do not know there is an alternative, that revenue is vulnerable. If a roaming package is expensive but hard to compare, it becomes exposed once eSIM marketplaces make pricing transparent.

READ MORE: How the eSIM Stack Works: Providers, APIs, Infrastructure Explained

Also at risk are weak eSIM resellers with no real differentiation. The market is getting crowded. A white-label storefront with generic plans, no brand trust and slow support will struggle as customers learn to compare providers more carefully.

The post-roaming economy rewards companies that own context, trust, distribution or infrastructure. It punishes companies that simply sit between the customer and the network without adding much value.

Conclusion

The post-roaming market will not belong to one type of company.

Travel eSIM brands are winning attention because they made the problem visible and solvable. API platforms are winning quietly because they let everyone else sell connectivity. Airlines, banks and travel apps are powerful because they own the customer moment. Operators still have network depth, but they need to package it with the speed and clarity of digital brands. Enterprise providers have a separate opportunity because business mobility is less about cheap data and more about governance.

The bigger trend is not “eSIM beats roaming.” It is that connectivity is moving from a telecom tariff into a travel, finance, software and enterprise experience. That is a much more serious shift.

Traditional roaming will remain. Some travelers will still use operator passes. Some companies will prefer established telecom contracts. In regulated markets like the EU, roaming already works well enough for many people. But outside those comfort zones, the old model is losing its automatic position.

The real power list is not about who has the lowest price per gigabyte this month. It is about who controls the moment when a customer asks, “How will I stay connected when I land?”

That question used to belong almost entirely to mobile operators. Now it belongs to whoever can answer it first, clearly, and without making the traveler feel stupid.