Huawei Reaches 41% Share in Global Telecom Equipment

Chinese telecom technology giant Huawei strengthened its position in the global telecom equipment market in 2025, reaching a record 41 percent revenue share in markets outside North America. The milestone highlights the company’s ability to adapt to geopolitical pressure while continuing to expand its footprint across much of the world.

According to new analysis from Dell’Oro Group, Huawei’s growth comes during a period of cautious recovery for the telecom infrastructure industry. After several difficult years marked by declining operator investment, the global telecom equipment market returned to growth in 2025.

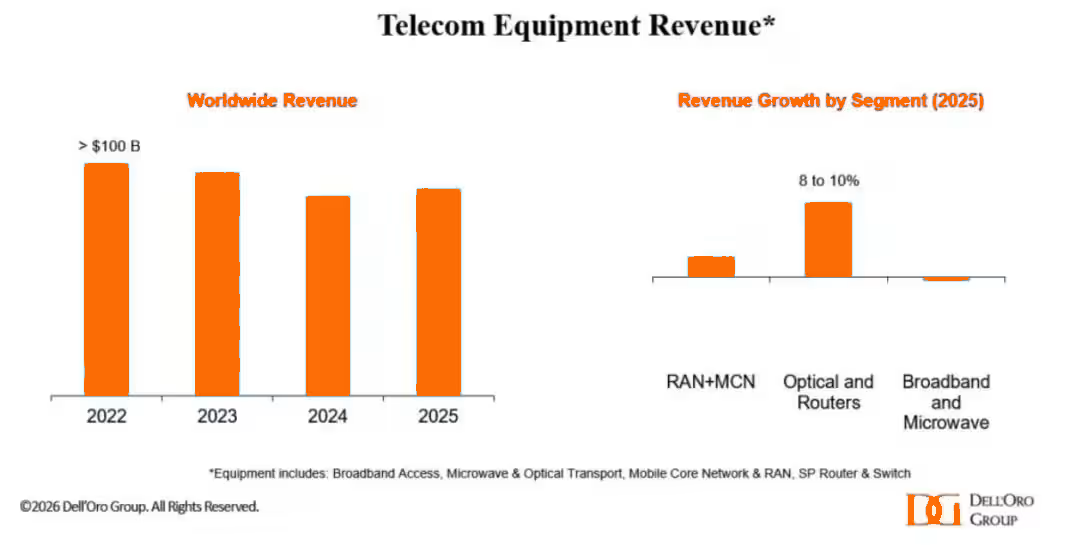

Worldwide telecom infrastructure revenue increased 4 percent year over year, reversing a prolonged downturn that saw the industry contract by 14 percent between 2022 and 2024.

Even with restrictions in several Western markets, Huawei has managed to strengthen its competitive position globally.

The top telecom network suppliers in 2025 include Huawei, Nokia, Ericsson, ZTE, Cisco, Ciena, Samsung, and HPE.

A Portfolio That Covers the Entire Network

One of the key reasons Huawei continues to lead the market is its unusually broad telecom portfolio.

According to Dell’Oro, the company ranks as the top supplier by revenue across all six major telecom infrastructure segments tracked by the research firm.

These segments include:

- Broadband Access

- Microwave and Optical Transport

- Mobile Core Network

- Radio Access Network (RAN)

- Service Provider Router and Switch

- Optical Networking

Very few telecom vendors can compete across the entire infrastructure stack.

While competitors like Ericsson and Nokia remain dominant in radio access networks, and companies such as Cisco and Ciena focus more heavily on routing and optical transport, Huawei operates across nearly every layer of telecom infrastructure.

For telecom operators, this offers a significant advantage. Instead of sourcing equipment from multiple suppliers, operators can deploy integrated networks built largely around a single vendor.

That approach simplifies network deployment, reduces integration complexity, and can accelerate the rollout of new services.

R&D Spending Still Drives Huawei’s Momentum

R&D Spending Still Drives Huawei’s Momentum

R&D Spending Still Drives Huawei’s Momentum

R&D Spending Still Drives Huawei’s MomentumAnother major factor behind Huawei’s continued success is its heavy investment in research and development.

The company consistently allocates a significant portion of annual revenue to R&D, one of the highest ratios among global telecom vendors. According to Huawei’s annual reports, the company has invested hundreds of billions of yuan in research over the past decade.

This investment has allowed Huawei to remain competitive in several critical areas of telecom technology.

These include:

High-capacity optical transport systems

Energy-efficient 5G base stations

Cloud-native mobile core networks

AI-driven network automation

Telecom operators are increasingly looking for technologies that can handle rapidly growing data traffic while reducing energy consumption and operating costs.

Huawei’s engineering focus in these areas has made its infrastructure solutions attractive to operators expanding their digital infrastructure.

Growing Influence Across Emerging Markets

While Huawei faces restrictions in parts of North America and several Western countries, the company has adapted by focusing on markets where it can compete freely.

Much of Huawei’s growth has come from Asia, the Middle East, Africa, and parts of Europe. These regions continue to invest heavily in telecom infrastructure as mobile usage, cloud services, and digital economies expand.

Many governments in emerging markets are prioritizing nationwide broadband coverage, 5G deployment, and fiber expansion. These projects often require large-scale infrastructure investments.

Huawei has positioned itself as a partner capable of delivering complete network solutions for these national connectivity initiatives.

By strengthening relationships with telecom operators and governments in these regions, the company has been able to offset restrictions in other markets.

Competition Looks Different Without North America

The structure of the telecom equipment market changes significantly depending on which regions are included in the analysis.

When China is excluded, the competitive landscape among vendors becomes more balanced.

However, when North America is removed from the equation, Huawei’s share increases dramatically. In those markets, the company reached 41 percent market share in 2025, according to Dell’Oro’s analysis.

This illustrates just how dominant Huawei remains across large parts of the global telecom ecosystem.

Demand for Next-Generation Networks Is Rising Again

Another factor supporting Huawei’s growth is the gradual recovery of telecom infrastructure spending.

After an intense wave of 5G investment earlier in the decade, many operators temporarily slowed network spending as they focused on monetizing those deployments.

But new digital demands are now pushing the next cycle of investment.

Operators worldwide are upgrading networks to support:

- 5G standalone architecture

- Fiber broadband expansion

- Cloud and edge computing connectivity

- Data center interconnection

These upgrades require modern optical transport systems, more advanced routing platforms, and scalable mobile core infrastructure.

In other words, telecom networks are becoming more software-driven, more cloud-integrated, and far more data-intensive than before.

That shift benefits vendors capable of delivering complete, integrated infrastructure platforms.

What This Means for the Telecom Equipment Market

Looking ahead, analysts expect the telecom infrastructure market to grow steadily but not explosively.

Dell’Oro Group forecasts 2 to 4 percent annual growth in 2026 across the six core telecom equipment segments.

Wireless infrastructure may grow more slowly than during the early 5G rollout, but demand for optical networking, routing, and data center connectivity is expected to remain strong.

Competition among vendors is also evolving.

Companies like Ericsson and Nokia continue to compete aggressively in radio access networks, while Cisco and Ciena dominate high-performance routing and optical transport in many Western markets. Samsung has also been increasing its presence in 5G infrastructure projects in selected regions.

Huawei, however, remains unusual among telecom vendors in its ability to deliver solutions across nearly every layer of the telecom network.

Conclusion

The telecom equipment market is no longer defined solely by technology leadership. It is increasingly shaped by geopolitics, regional alliances, and operator investment cycles.

Huawei’s rise to a 41 percent share outside North America reflects how the company has adapted to those realities.

Rather than retreating from global competition, Huawei has doubled down on research investment, expanded partnerships across emerging markets, and leveraged its broad technology portfolio to remain central to global network deployment.

For telecom operators building the next generation of digital infrastructure, the choice of vendor is no longer just about price or performance. It is also about ecosystem compatibility, regulatory environments, and long-term strategic alignment.

In that complex landscape, Huawei’s ability to compete across nearly the entire telecom stack ensures it will remain one of the most influential players in the global connectivity industry for years to come.