The eSIM Store Is Everywhere Now

Not long ago, selling an eSIM was relatively straightforward: you built a website, integrated with a connectivity provider, and waited for travelers to Google “eSIM for Europe.” That window is closing fast. The channel stack has exploded — and the companies that understand where distribution is heading are quietly building moats while others are still optimizing landing pages.

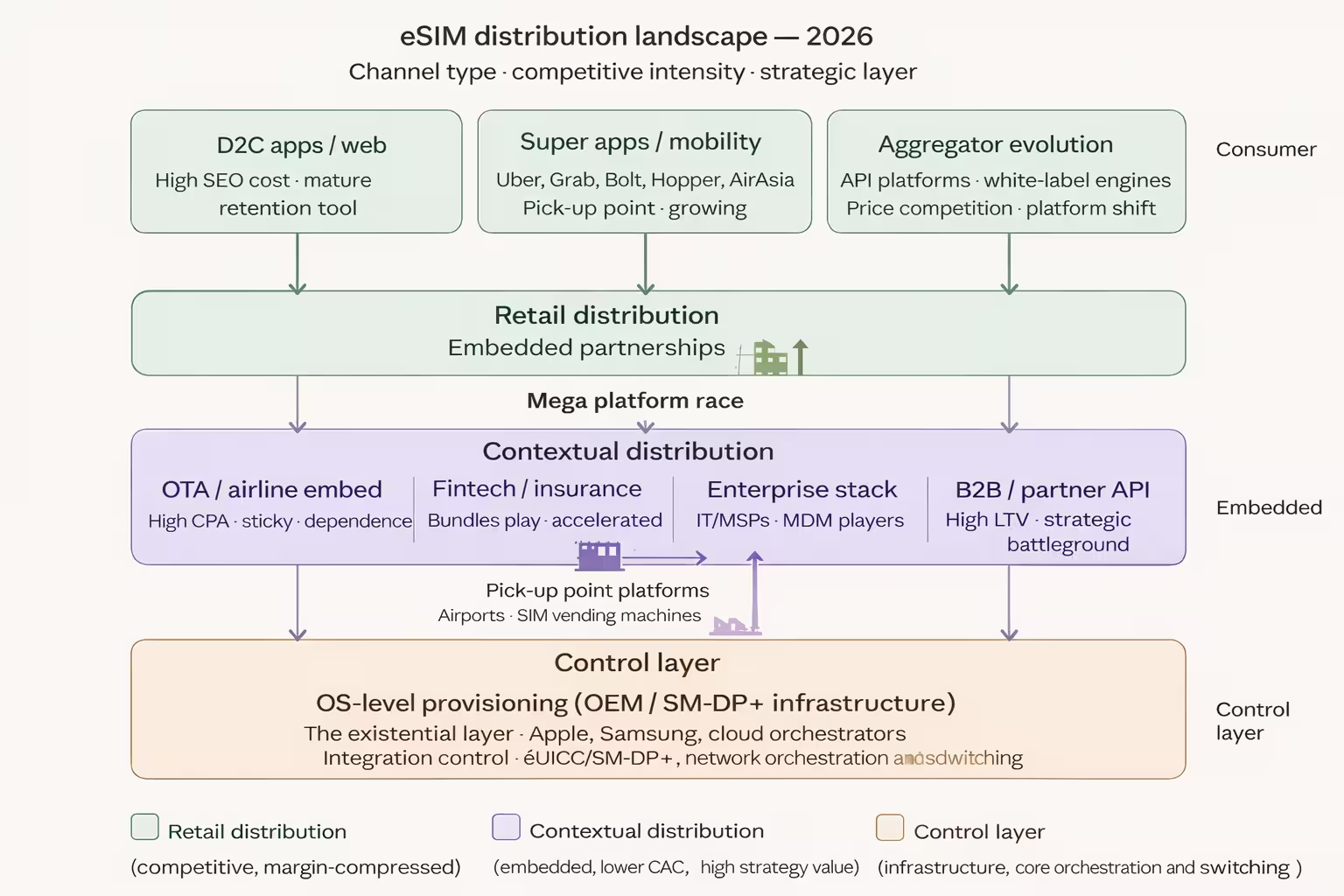

Today, eSIM is sold through at least seven distinct channel types, each with its own economics, conversion logic, and competitive dynamics. Understanding them isn’t just an academic exercise. It’s the difference between a sustainable connectivity business and a perpetual customer acquisition treadmill.

Where It Actually Moves Today

The direct-to-consumer web store is still the backbone for most standalone eSIM providers — Airalo, Holafly, Nomad, and Yesim all built their brands here. SEO is the primary acquisition lever, and it’s brutal. Cost-per-click on high-intent travel connectivity keywords has risen sharply, and the top positions are increasingly dominated by a handful of players with seven-figure content budgets. For newer entrants, organic search is a slow build. Paid search often doesn’t pencil out.

App-native sales are where the consumer brands are doubling down. Airalo’s app is arguably its real product at this point — the eSIM is almost secondary to the UX, the loyalty mechanics, and the push notification infrastructure they’ve built around it. Holafly has moved similarly. When a user already has your app on their phone, the conversion funnel collapses dramatically. You don’t need Google anymore.

That said, calling the app the product is a stretch. The real product is still coverage, pricing, and reliability on the ground. The app is what improves distribution and retention — not what defines the core value.

Then there’s the embedded channel — and this is where things get genuinely interesting. OTA platforms like Booking.com, Expedia, and Kiwi.com are starting to bundle connectivity into the checkout flow. Travel insurance companies are experimenting with it. Airlines remain structurally slower due to integration and ownership complexity, but a few — particularly in Asia and the Middle East — have launched or piloted eSIM add-ons. Conversion varies widely by placement and timing, but the volumes can be enormous, and the CAC shifts from upfront spend to revenue share and platform dependency.

The B2B and corporate travel channel is underdeveloped relative to its potential. Yesim has been the most deliberate about it, with its OneBalance product and a Partner API that lets companies provision connectivity for employees without going through a consumer-facing flow. Ubigi has taken a similar approach, leaning into device-maker partnerships (notably with Lenovo) and corporate data management. Most of the pure-play consumer eSIM brands have ignored this segment almost entirely — which is either a blind spot or a strategic choice, depending on who you ask.

Finally, there’s the device-level channel: eSIMs activated at setup, bundled with a new phone or tablet, increasingly pre-provisioned by carriers. This is the channel that could eventually disintermediate everyone else, and it’s worth taking seriously.

Infrastructure is where the real power is consolidating

The real shift in control is happening one layer deeper — in the systems that decide how connectivity is provisioned, routed, and delivered.

- Orchestration platforms that dynamically select networks and manage switching logic across regions

- SM-DP+ providers controlling how eSIM profiles are created, distributed, and activated at scale

- API-first telecom platforms turning connectivity into a service that can be embedded into banks, airlines, travel platforms, and enterprise systems

This is the layer most consumer eSIM brands never touch. They operate on top of it, not within it.

And that distinction matters.

Because over time, control shifts away from whoever owns the customer interface and toward whoever controls provisioning, policy, and network logic underneath.

👉 The companies that own orchestration and provisioning don’t just participate in distribution. They define it.

The Affiliate Machine — And Its Limits

It would be incomplete to talk about eSIM distribution without acknowledging the affiliate ecosystem. Travel bloggers, YouTube creators, and comparison sites have been a meaningful acquisition channel for mid-tier eSIM brands — particularly for providers who can’t compete on brand awareness with Airalo. The challenge is structural: affiliate economics reward whoever has the best commission rate, not the best product. It trains a price-sensitive audience, generates low loyalty, and creates a revenue base that can evaporate the moment a larger competitor raises their payout floor.

Some providers have tried to counter this with co-branded content partnerships — essentially content-to-commerce hybrids where the editorial layer adds context and comparison rather than just a coupon code. Alertify’s own model leans into this: the combination of genuine coverage and commercial relationships means readers arrive with some baseline trust, rather than just responding to a discount prompt. It’s a more durable model, but it requires actual editorial investment.

The Battle Nobody’s Winning Yet

Corporate travel is the biggest distribution gap in the market right now. According to GBTA data, global business travel spend is back above pre-pandemic levels, and connectivity is increasingly a line item that companies want to manage centrally rather than leave to individual employees expensing whatever they bought at the airport. The eSIM providers best positioned to capture this are the ones with proper API infrastructure, multi-user account management, and the ability to integrate with tools like SAP Concur or TravelPerk — not the ones with the most Instagram followers.

Yesim’s OneBalance product is the most complete attempt at this so far among the consumer-adjacent brands. 1GLOBAL operates at a different altitude — licensed infrastructure across 42 countries, enterprise clients like Revolut and N26 — but that’s a different product category entirely. The gap in the middle (SME and mid-market corporate) is essentially uncontested.

The Real Conclusion

The eSIM distribution story of the next three years is fundamentally a story about who can exit the direct-response consumer acquisition loop. Airalo has done it more successfully than anyone — their app installed base and loyalty program mean they’re less dependent on Google than any other player in the space. Holafly is close behind on the consumer side. Neither has established leadership in embedded or B2B

The more instructive comparison might be with what happened in travel insurance — a product with a similar profile (low engagement, high intent at point of purchase, strong bundling potential). Players like Battleface and SafetyWing didn’t try to out-SEO Allianz. They went API-first, embedded into booking flows, and built distribution through partnerships rather than search. That playbook is available to eSIM providers, and it’s surprisingly underutilized.

What the GSMA’s data on eSIM adoption trajectories consistently shows is that activation complexity — not price — is the primary barrier to mainstream uptake. That means whoever reduces friction at the moment of purchase (whether that’s an OTA checkout, a bank app, or a device setup screen) wins, regardless of the underlying product specs. Distribution, not product, is the competitive surface area that matters most now. And increasingly, connectivity is no longer even sold — it’s embedded.

The providers still optimizing their meta descriptions should probably be studying their partnership pipeline instead.