EU Approves Apple’s Plan to Open iPhone Tap-to-Pay to Rivals

The European Commission has made commitments offered by Apple legally binding under EU antitrust rules. The commitments address the Commission’s competition concerns relating to Apple’s refusal to grant rivals access to a standard technology used for contactless payments with iPhones in stores (‘Near-Field-Communication (NFC)’ or ‘tap and go’). Apple iPhone tap-to-pay EU access

This move ends a lengthy investigation and spares Apple a hefty fine, but what does it mean for consumers and competitors alike?

Apple’s Monopoly in Mobile Payments

Apple Pay is Apple’s own mobile wallet used to allow iPhone users to pay with their devices in stores and online. Apple’s iPhones run exclusively on Apple’s operating system ‘iOS’. Apple controls every aspect of its ecosystem, including access conditions for mobile wallet developers.

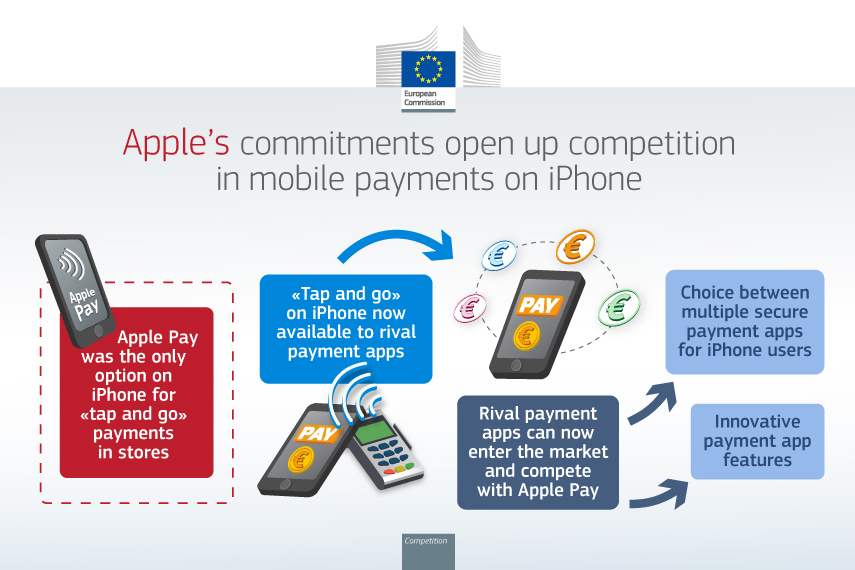

The Commission preliminarily found that Apple has significant market power in the market for smart mobile devices and a dominant position on the in-store mobile wallet market on iOS. Apple Pay is the only mobile wallet that may access the NFC hardware and software (‘NFC input’) on iOS to make payments in stores, as Apple does not make it available to third-party mobile wallet developers.

In its investigation, the Commission preliminarily concluded that Apple abused its dominant position by refusing to supply the NFC input on iOS to competing mobile wallet developers while reserving such access only to Apple Pay.

For years, Apple Pay has been the go-to mobile payment solution for iPhone users. With its seamless integration and robust security features, it’s no surprise that Apple Pay has dominated the market. However, this dominance has not gone unnoticed by regulatory bodies, particularly in the EU. Apple iPhone tap-to-pay EU access

The EU’s Stance on Competition

The European Union, known for its stringent regulations and pro-competition stance, launched a probe into Apple’s practices. The concern was clear: Apple’s exclusive control over the iPhone’s tap-to-pay technology was stifling competition and limiting consumer choices.

The Decision: Opening the Doors

The EU’s Approval

On a significant Thursday, the EU approved Apple’s proposal to allow rival companies access to its iPhone tap-to-pay capabilities. This decision marks the end of the investigation and is seen as a victory for both competitors and consumers.

Margrethe Vestager, the EU competition chief, emphasized the benefits of this decision. “From now on, competitors will be able to effectively compete with Apple Pay for mobile payments with the iPhone in shops. So consumers will have a wider range of safe and innovative mobile wallets to choose from,” she said.

Apple commitments

To address the Commission’s competition concerns, Apple initially offered the following commitments:

- To allow third-party wallet providers access to the NFC input on iOS devices free of charge, without having to use Apple Pay or Apple Wallet. Apple will enable access to NFC in Host Card Emulation mode (‘HCE‘). HCE allows to securely store payment credentials and complete transactions using NFC, without relying on an in-device secure element.

- To apply a fair, objective, transparent and non-discriminatory procedure and eligibility criteria to grant NFC access to third-party mobile wallet app developers.

- To enable users to easily set an HCE payment app as their default app for payments in stores and to use relevant functionalities such as Field Detect (which opens the user’s default payment app when a locked iPhone is presented to an NFC reader), Double-click (which launches the default payment app when double clicking the phone’s side or home button), and authentication tools such as Touch ID, Face ID, and device passcode.

- To establish a monitoring mechanism and separate dispute settlement system to allow for independent review of Apple’s decisions restricting access.

- To apply the abovementioned commitments to all third-party mobile app developers established in the European Economic Area (‘EEA’) and to all iOS users with an Apple ID registered in the EEA, also while traveling temporarily outside the EEA.

Between 19 January 2024 and 19 February 2024, the Commission market tested Apple’s commitments and consulted all interested third parties to verify whether they would remove its competition concerns. In light of the outcome of this market test, Apple amended the initial proposal and committed:

- To extend the possibility to initiate payments with HCE payment apps at other industry-certified terminals, such as merchant phones or devices used as terminals (so called SoftPOS), if this is enabled.

- To explicitly acknowledge that HCE developers are not prevented from combining the HCE payment function with other NFC functionalities or use cases.

- To remove the requirement for developers to have a license as a Payment Service Provider (‘PSP’) or a binding agreement with a PSP to access the NFC input.

- To allow NFC access for developers to pre-build payment apps for third-party mobile wallet providers.

- To update the HCE architecture to comply with evolving industry standards used by Apple Pay, and to continue to update standards even if they are no longer implemented by Apple Pay, under certain conditions.

- To enable developers to prompt users to easily set up their default payment app and redirect users to the default NFC settings page, enabling defaulting with only a few clicks.

- To comply with the same industry standard-specifications as developers of HCE payment apps and to protect confidential information obtained in the context of an audit.

- To shorten deadlines for resolving disputes. Moreover, Apple offered additional independence and procedural guarantees for the monitoring trustee.

The Commission concluded that Apple’s final commitments would address its competition concerns over Apple’s restriction of third-party mobile wallet developers’ access to NFC payments in stores for EEA iOS users. It therefore decided to make them legally binding on Apple.

The commitments will remain in force for 10 years and apply throughout the EEA. Their implementation will be monitored by a monitoring trustee appointed by Apple who will report to the Commission for the same time period.

Apple’s commitments are without prejudice to Apple’s current or future obligations under other regulations, in particular relating to other use cases and functionalities within the scope of the Digital Markets Act (Regulation 2022/1925) and the implementation of the Digital Euro.

What This Means for Competitors

Leveling the Playing Field

Competitors like Google Pay and Samsung Pay now have the opportunity to integrate their services with the iPhone’s NFC (Near Field Communication) technology. This integration is expected to foster innovation and provide consumers with more choices.

Potential Challenges

While this move is promising, it is not without challenges. Competitors must ensure their payment solutions are as seamless and secure as Apple Pay to win over iPhone users. Apple iPhone tap-to-pay EU access

Impact on Consumers

More Choices, Better Services

Consumers stand to gain the most from this decision. With multiple mobile wallet options available, users can choose the service that best suits their needs. This competition is likely to lead to better features, enhanced security, and possibly lower transaction fees.

Ensuring Security

Security remains a top priority. Any new mobile wallet entering the iPhone ecosystem must adhere to strict security protocols to protect user data and prevent fraud.

The Future of Mobile Payments

A New Era of Innovation

The opening of iPhone’s tap-to-pay functionality is expected to spur innovation in the mobile payment sector. Companies will be motivated to develop new features and services to differentiate themselves from the competition.

The Role of Fintech Startups

Fintech startups, in particular, may find new opportunities in this evolving landscape. With access to the iPhone’s NFC technology, these companies can experiment with cutting-edge payment solutions and potentially disrupt the market.

Conclusion: A Win for Competition and Consumers

The EU’s decision to approve Apple’s plan is a significant step towards a more competitive and consumer-friendly mobile payment market. By allowing rivals access to its tap-to-pay technology, Apple has opened the doors to innovation and choice. As we move forward, we can expect a dynamic and evolving landscape that benefits everyone involved. Apple iPhone tap-to-pay EU access