eSIM RSP Platforms: Who Leads in 2026?

If you felt that the eSIM ecosystem moved from “interesting” to “inevitable” over the past year, the numbers now confirm it.

According to Counterpoint Research’s latest GIobal eSIM Provisioning Landscape Report, transactions across eSIM Remote SIM Provisioning platforms grew nearly 1.4x year over year in 2025. That is not incremental growth. That is structural acceleration.

And the primary driver? Travel eSIM.

For those of us watching the travel connectivity segment closely, this will not come as a surprise. What is more interesting is how this consumer-facing growth is now reshaping the competitive hierarchy of the provisioning layer behind it.

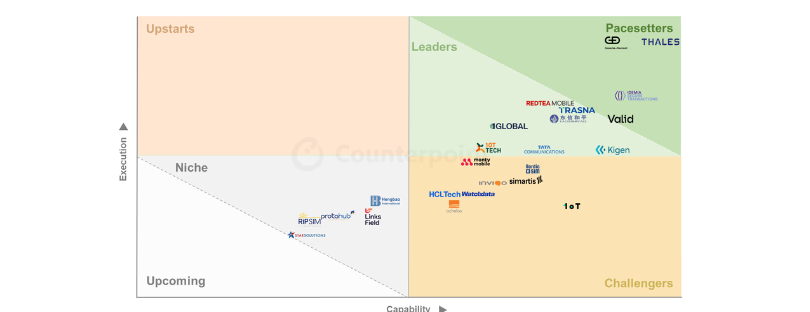

The CORE Rankings Explained

Counterpoint’s Global eSIM Provisioning Competitive Ranking and Evaluation, known as CORE, maps vendors across two dimensions: platform capability and market execution.

Capability looks at technical depth. This includes GSMA-certified components, SGP.32 readiness, eSIM IoT Manager support, automation maturity, security frameworks, interoperability breadth, and backend architecture.

Execution measures real-world traction. Live deployments. Transaction volumes. Customer scale. Geographic footprint.

Together, these dimensions offer a rare structured look into what is often an opaque infrastructure layer of the eSIM ecosystem.

Pacesetters: The Top Tier

Pacesetters: The Top Tier

Pacesetters: The Top Tier

Pacesetters: The Top TierThis year, Thales, Giesecke+Devrient (G+D), IDEMIA and Valid emerged as Pacesetters.

Research Director Mohit Agrawal summarized it clearly:

“Thales, G+D and IDEMIA have once again emerged as Pacesetters in the eSIM provisioning rankings, maintaining their top-tier positioning for the sixth consecutive year. Thales secured the highest overall placement with its well-rounded platform capabilities across consumer and IoT provisioning. G+D demonstrated strong execution momentum, narrowly leading in live deployments and transaction volumes.”

Valid’s move into the Pacesetters quadrant is particularly notable. It marks a first for the company and signals a broader geographic diversification in leadership within the provisioning market. Its strengthened SGP.32-focused platform capabilities and improved execution metrics were key drivers.

For the first time, SGP.32 readiness is no longer a roadmap slide. It is influencing rankings.

Leaders: Strong Execution, Expanding Footprint

In the Leaders quadrant, we see Trasna, Eastcompeace, RedTea Mobile, Kigen, 1GLOBAL, Tata Communications and 10T Tech.

10T Tech’s advancement into the Leaders quadrant reflects improved execution metrics. Eastcompeace recorded one of the strongest year-on-year increases in deployment activity. Kigen continues to differentiate with platform capabilities that approach the upper tier.

What stands out here is the blend of heritage telecom groups, IoT-native players, and digital-first eSIM specialists. The provisioning market is no longer dominated by a single profile of vendor.

Challengers and Niche Specialists

Monty Mobile, Watchdata and HCLTech moved from Niche into the Challengers quadrant. Their progress reflects strengthened architecture, security, and interoperability capabilities.

Within this segment, Monty Mobile also recorded notable growth in deployments and transaction volumes, signaling execution momentum rather than pure technical expansion.

Meanwhile, Achelos, Invigo and Nordic eSIM retained Niche positioning. These companies typically operate with focused regional strategies or specialized service models. They do not compete full-stack. They specialize.

And in a maturing market, specialization is not weakness. It is strategy.

Travel eSIM: The Unexpected Growth Engine

Senior Analyst Varun Gupta put it directly:

“In 2025, eSIM Remote SIM Provisioning (RSP) platforms recorded around 1.4x growth in transaction volumes across consumer and IoT deployments, largely driven by the rapid expansion of travel eSIM services. Some vendors reported significantly high growth, even doubling their transactions, highlighting accelerating consumer awareness and adoption of travel eSIM offerings. The expansion of eSIM-only smartphone portfolios, including broader geographic availability of eSIM-only models from Apple, further contributed to transaction growth in the latter half of the year. At the ecosystem level, nearly half of the vendors ranked in the CORE assessment now report certified eSIM IoT Manager (eIM) capabilities, while over half are conducting pilots or early-stage deployments. This indicates that SGP.32-based provisioning is transitioning from roadmap positioning to early commercialization, laying the foundation for the next phase of eSIM ecosystem expansion.”

That paragraph alone captures the structural shift.

Travel eSIM is no longer a niche product sold to digital nomads. It is driving provisioning transaction growth at infrastructure scale.

And eIM plus SGP.32 readiness signals that the IoT wave is preparing to follow.

SGP.32: From Specification to Commercial Reality

The GSMA’s SGP.32 specification is central to the next phase of eSIM evolution. Unlike SGP.22, which primarily serves consumer devices, SGP.32 is designed for IoT-scale remote provisioning with enhanced orchestration and lifecycle management.

Nearly half of CORE-ranked vendors now report certified eIM capabilities. More than half are piloting or early-deploying SGP.32-based solutions.

That is not theoretical progress. That is ecosystem preparation.

As Gupta noted, vendors are moving beyond compliance-driven deployments toward orchestrated, scalable platforms designed to support growing transaction volumes.

Translation: certification alone is no longer enough. Depth, automation, security, and backend unification are the new battleground.

The Bigger Picture: Infrastructure Maturity

When you step back, the rankings reveal a deeper pattern.

The eSIM provisioning market is transitioning from:

- Compliance-driven deployment

- Certification as competitive edge

- Fragmented consumer and IoT backends

Toward:

- Unified orchestration platforms

- Automation-led provisioning workflows

- Security and interoperability as differentiators

- Execution scale as validation

This mirrors what we have seen in adjacent markets. In cloud infrastructure, in API management, in payment processing. Early winners were those who certified first. Long-term leaders are those who scale best.

Provisioning is no longer a background technical function. It is becoming programmable connectivity infrastructure.

How This Compares to Broader Market Trends

Industry data from the GSMA Intelligence and multiple OEM shipment reports have consistently shown double-digit eSIM device growth globally. Apple’s eSIM-only expansion in additional markets accelerated consumer awareness in 2025. Android OEMs continue broadening eSIM-first portfolios.

At the same time, enterprise IoT deployments are scaling. Fleet management, asset tracking, industrial monitoring and connected healthcare all require secure, remote, lifecycle-managed connectivity.

The CORE rankings reflect that convergence.

Consumer growth built volume. IoT readiness is building complexity.

Vendors who can handle both will define the next phase.

What This Means for the Ecosystem

If you are an operator, this ranking matters because provisioning partners increasingly influence your speed to market.

If you are an IoT platform provider, SGP.32 maturity will determine how scalable your device lifecycle management becomes.

If you are in travel eSIM, you may not see the provisioning layer directly, but it is the backbone enabling instant activation, multi-country switching, and profile orchestration.

The fact that transaction volumes grew 1.4x year over year tells us something fundamental: eSIM has crossed from adoption to acceleration.

Conclusion

The 2026 CORE rankings do more than shuffle vendor positions. They reveal a market that is expanding in both scale and sophistication.

Travel eSIM drove the volume spike. eSIM-only smartphones reinforced consumer normalization. SGP.32 and eIM readiness signal IoT’s commercial takeoff.

What differentiates vendors now is not certification alone, but platform depth, orchestration capability, automation maturity, security robustness, and measurable execution.

Compared with adjacent infrastructure markets and supported by GSMA and OEM shipment data, the trajectory is clear. eSIM provisioning is evolving into a strategic infrastructure layer rather than a compliance utility.

The winners of the next five years will not be those who simply deploy profiles. They will be those who orchestrate connectivity at scale, across consumer and IoT domains, with resilience and automation built in.

The market is no longer asking who can provision.

It is asking who can scale.